Roth IRA vs. Traditional IRA: Which Account Fits Your Tax Situation?

Compare tax treatment, contribution limits, and withdrawal rules to choose Roth, traditional, or a mix for retirement savings.

The One Difference That Matters

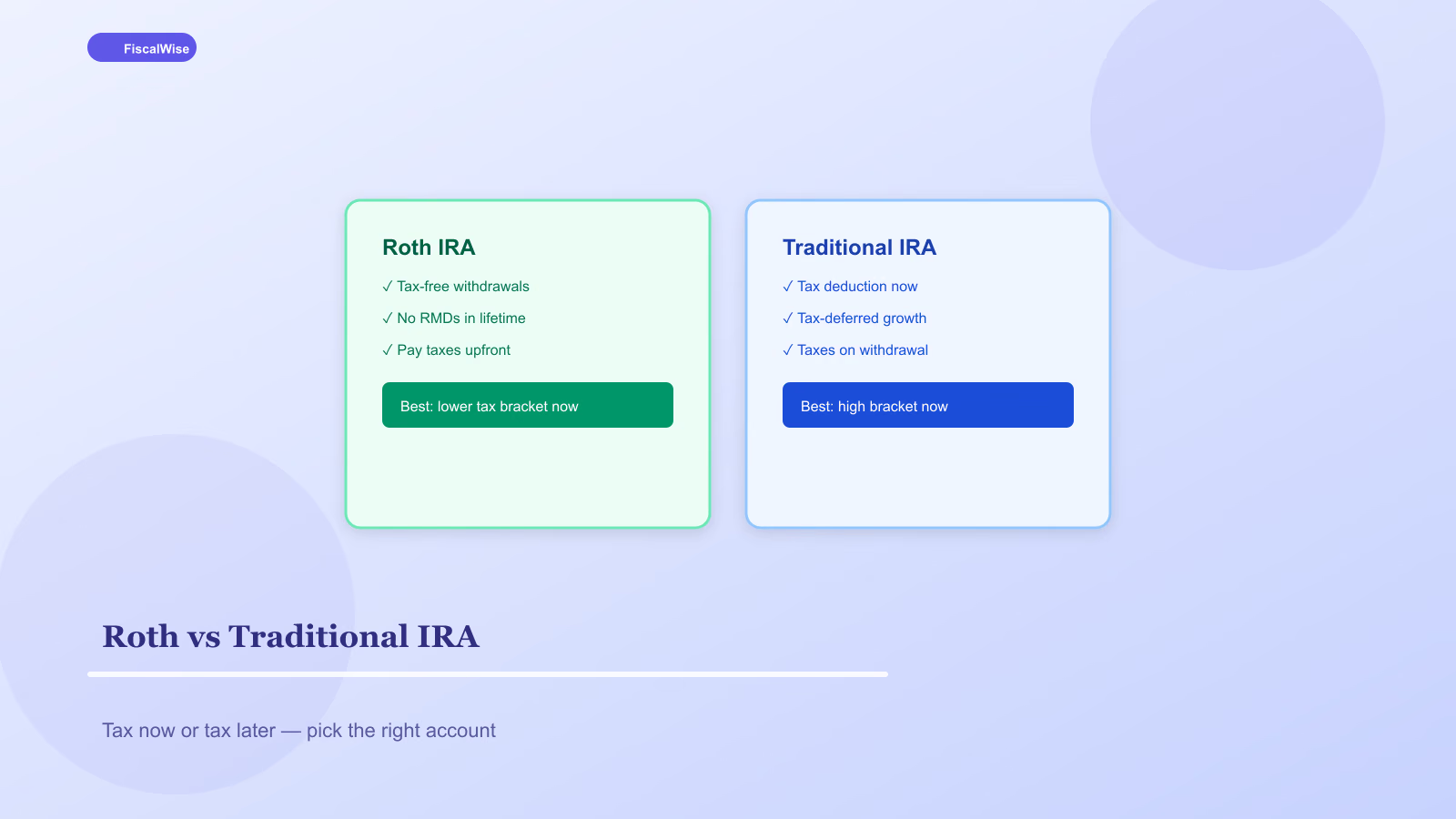

Traditional IRA contributions may be tax-deductible now; you pay ordinary income tax on withdrawals in retirement. Roth IRA contributions are made with after-tax dollars; qualified withdrawals — including investment growth — are tax-free.

The choice is a bet on your tax rate now vs. later. Lower rate today than in retirement? Traditional deduction helps. Higher rate later, or you want tax-free legacy? Roth wins.

Side-by-Side Comparison

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Tax break | Often upfront deduction | None upfront |

| Growth | Tax-deferred | Tax-free if qualified |

| Withdrawals | Taxed as income | Tax-free after 59½ + 5-year rule |

| RMDs | Required at 73+ | No RMDs for original owner |

| Income limits | Deduction phases out with workplace plan | Contribution phases out at higher incomes |

Check current IRS limits annually — our retirement savings calculator projects growth; contribution caps are updated in tax guides each year.

Who Should Favor Traditional

- High earners in peak tax brackets who need deduction room

- Workers without Roth 401(k) who want immediate tax relief

- People expecting lower income in retirement — smaller bracket, same state

Run marginal rate estimates with our tax bracket calculator before assuming the deduction beats Roth.

Who Should Favor Roth

- Young workers in lower brackets — pay tax now at 12–22% vs. unknown future rates

- Savers who max workplace plans and want tax diversification

- Anyone who values tax-free inheritance for heirs (rules apply)

- Early-career households expecting income to climb

Tax Diversification: Why Not Both

Retirement tax risk is unknown — Congress, state moves, RMDs pushing you into higher brackets. Holding traditional, Roth, and taxable accounts creates flexibility:

- Live on Roth in years with extra income spikes

- Use traditional when income is low

- Harvest taxable lots strategically

Conversion Strategies

Roth conversions move traditional IRA dollars to Roth, paying tax now. Popular in low-income years — career break, early retirement before Social Security, layoff year. Spread large conversions across tax years to avoid jumping brackets.

Model conversion cost with the tax bracket calculator — converting $40,000 might fill the 22% bucket but push the next dollar into 24%.

Withdrawal Rules You Cannot Ignore

Traditional: 10% penalty on most withdrawals before 59½, plus tax. Exceptions exist for first home, education, SEPP — read IRS guidance.

Roth: Contributions can be withdrawn anytime tax-free — growth cannot without penalty until qualified. Five-year clock applies per conversion.

Workplace Plan Interaction

If you have a 401(k), IRA deductibility may phase out by income. You can still contribute non-deductible traditional and consider backdoor Roth — advanced move with pro-rata rule pitfalls; consult a CPA if balances are mixed.

Projecting Outcomes

Same $6,500 annual contribution for 30 years at 7% growth:

- Traditional saves taxes upfront each year

- Roth pays tax now but $X grows tax-free

Which wins depends on rate differential. Our investment return calculator and retirement projection tools help stress-test assumptions — not predict Congress.

Practical Decision Flow

- Get employer 401(k) match first — free money

- If in low bracket, fund Roth IRA

- If need deduction, fund traditional IRA or increase 401(k) pre-tax

- Max available tax-advantaged space

- Taxable brokerage for overflow

Roth vs. traditional is not loyalty oath — it is tax timing. Pick what matches this decade's bracket, revisit after major life changes, and build both when you can.

Topics covered

- Roth IRA

- traditional IRA

- retirement accounts

- tax planning

Frequently Asked Questions

Can I contribute to both a Roth and traditional IRA?

Yes, but combined contributions cannot exceed the annual IRA limit. Tax deductibility of traditional contributions may phase out if you have a workplace retirement plan and income above IRS thresholds.

When does a Roth IRA make more sense than traditional?

Roth often wins when you are in a lower tax bracket now than you expect in retirement, want tax-free withdrawals, or value tax-free inheritance for heirs. Young workers in the 12–22% bracket are common Roth candidates.

What is a Roth conversion?

Moving money from a traditional IRA to a Roth by paying income tax now. Popular in low-income years — career breaks, early retirement before Social Security — to fill lower tax brackets deliberately.

Are Roth IRA withdrawals always tax-free?

Contributions can be withdrawn anytime tax-free. Earnings require you to be 59½ and meet the five-year rule for qualified tax-free withdrawals. Non-qualified earnings withdrawals may trigger tax and penalty.