Japan NISA Investing Guide: New NISA, iDeCo, and Tax-Free Growth

How Japan's New NISA tax-free investment accounts work, annual limits, growth vs tsumitate plans, and pairing with iDeCo retirement savings.

Why NISA Matters for Japanese Investors

Japan taxes investment gains and dividends in taxable accounts. NISA (Nippon Individual Savings Account) wraps qualifying investments so profits and distributions are tax-free for the holding period — a rare edge in a low-rate, cash-heavy savings culture.

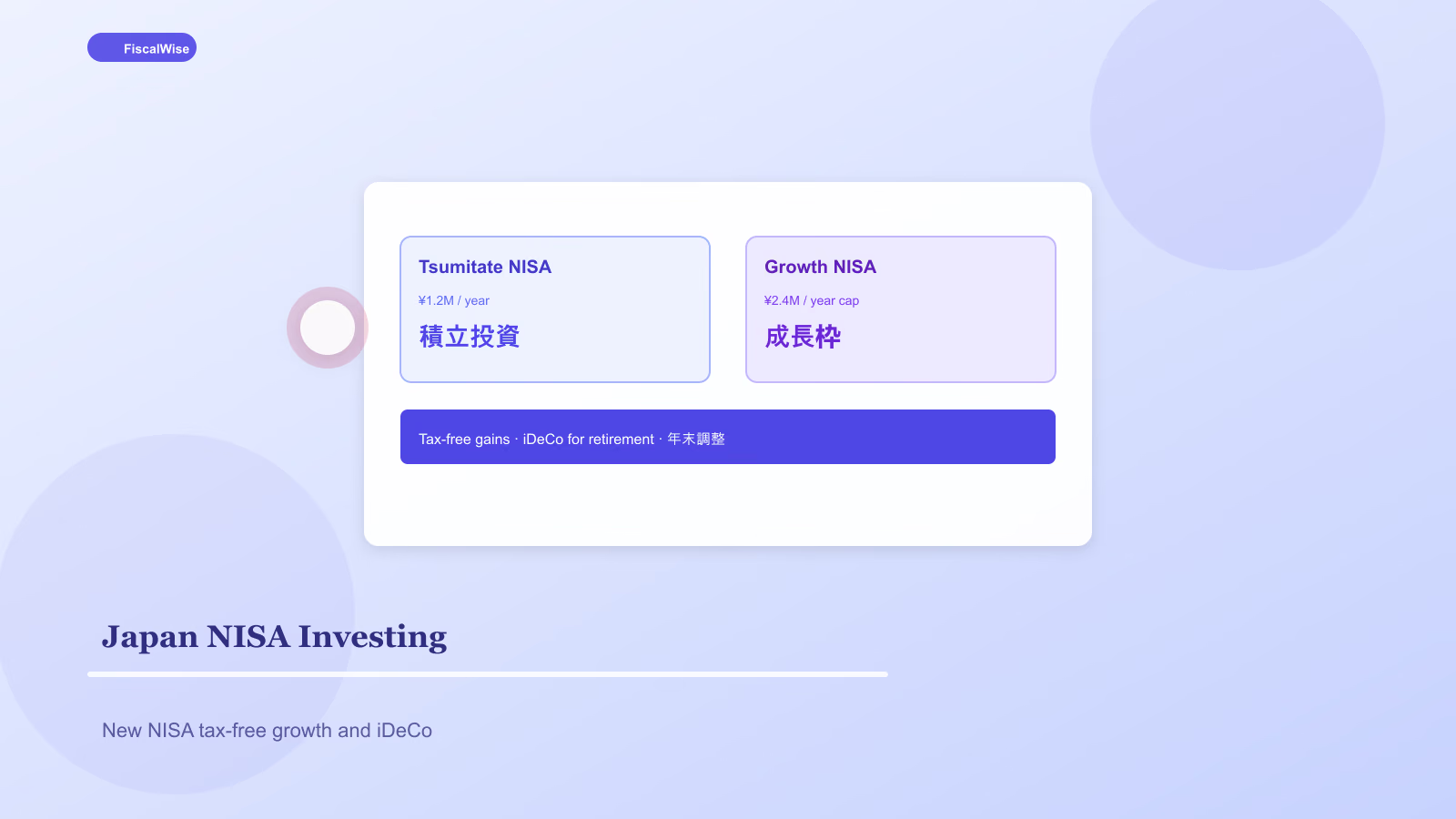

Since 2024, New NISA replaced the old system's confusing renewal rules with simpler lifetime caps and two main buckets:

| Plan | Annual limit | Lifetime cap | Best for |

|---|---|---|---|

| --- | ---: | ---: | --- |

| **Tsumitate (accumulation)** | ¥1.2 million | No lifetime cap | Monthly index funds, investment trusts |

| **Growth** | ¥2.4 million | ¥12 million total | Lump sums, broader product range |

You can use both in the same year within their respective limits.

Tsumitate vs Growth: Which to Use First

Tsumitate NISA suits beginners — automatic monthly purchases of eligible investment trusts, often low-cost index funds. Dollar-cost averaging (積立) matches paycheck rhythm and reduces timing anxiety.

Growth NISA accepts wider products including certain stocks and ETFs, subject to eligibility lists. Useful for lump-sum bonuses after emergency fund and short-term goals are covered.

Most households start tsumitate, add growth when comfortable.

What to Buy Inside NISA

Boring wins:

- Low-cost global or developed-market index funds

- Domestic equity index if home bias preferred

- Avoid high-fee active funds that eat the tax benefit

NISA tax-free status does not prevent losses — a −30% fund is still −30%. Match equity exposure to money you will not need for 10+ years.

Project long-term outcomes with our compound interest calculator and investment return calculator.

iDeCo: Retirement Layer Beyond NISA

iDeCo (individual-type Defined Contribution pension) offers tax-deductible contributions, tax-free growth, and taxation only on withdrawal — typically at lower rates in retirement.

| Feature | NISA | iDeCo |

|---|---|---|

| Access | Anytime (with product rules) | Generally age 60+ |

| Tax on contributions | After-tax | Deductible |

| Tax on growth | Free | Free |

| Withdrawal tax | Free | Taxed as income |

iDeCo locks money until 60 (with exceptions). NISA is flexibility; iDeCo is retirement discipline. Many salaried workers use both.

Contribution limits depend on employment status — company employees have lower caps than self-employed; check current 年金機構 tables.

Year-End Tax Adjustment (年末調整)

Salaried employees see iDeCo deductions reflected through employer year-end adjustment in November–December. Open iDeCo and set contributions early in the calendar year to spread cash flow — not a December scramble.

Common Mistakes

Cash sitting outside NISA for years — Tax drag compounds; start tsumitate small.

Churning funds inside NISA — Trading burns returns; pick and hold.

Maxing growth NISA with speculative stocks — Tax-free gambling is still gambling.

Skipping iDeCo because NISA exists — Different jobs; retirement needs both liquidity and locked savings.

Broader Japanese Household Finance

Before aggressive NISA funding:

- Emergency fund — 3–6 months expenses in ordinary deposit account

- Debt — Pay high-interest card balances (Japan cards can exceed 15% APR)

- Insurance — Separate term life and medical from investment-linked products

Use our emergency fund calculator with yen formatting via the currency selector on any calculator page.

New NISA simplified Japan's tax-free investing lane. Automate tsumitate, respect growth caps, pair with iDeCo for retirement, and let decades of tax-free compounding do the work.

Topics covered

- NISA Japan

- New NISA

- iDeCo

- Japan investing

- tsumitate NISA

Frequently Asked Questions

What is the New NISA annual limit?

Tsumitate NISA allows up to ¥1.2 million per year in eligible accumulation products. Growth NISA allows up to ¥2.4 million per year with a ¥12 million lifetime cap.

What is the difference between NISA and iDeCo?

NISA offers tax-free investment growth with flexible access. iDeCo offers tax-deductible contributions and tax-free growth but locks funds until generally age 60. They serve different roles.

Can I lose money in a NISA account?

Yes. NISA only eliminates tax on gains and dividends — it does not protect against market losses. Invest according to your time horizon and risk tolerance.

Should I start with tsumitate or growth NISA?

Most beginners start with tsumitate NISA for automatic monthly index fund purchases, then use growth NISA for lump sums once emergency savings and debt are under control.