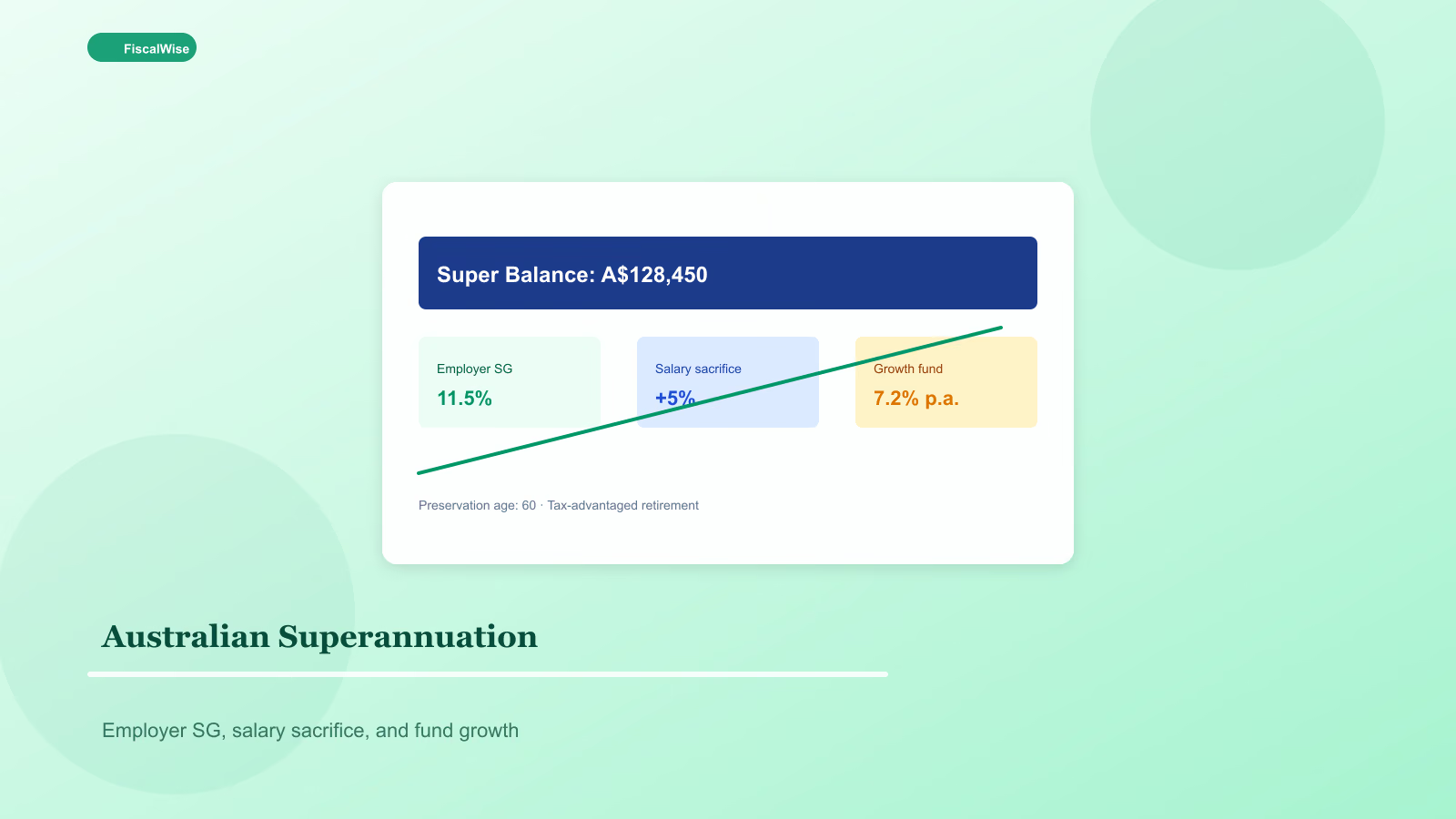

Australian Superannuation Basics: How Your Retirement Fund Works

Employer contributions, salary sacrifice, investment options inside super, and when to make voluntary top-ups before EOFY.

What Superannuation Is

Superannuation ("super") is Australia's compulsory retirement savings system. Employers must pay 11.5% of ordinary time earnings (rate rises gradually toward 12%) into a super fund for eligible employees. That money is invested until you reach preservation age and meet a condition of release — typically retirement from age 60.

Unlike cash in a bank account, super is illiquid for decades. That is the point: compound growth on money you cannot touch for lunch.

Your Super Account: What to Check First

Log into your fund portal and confirm:

- Which fund holds your balance — many Australians have multiple accounts from job changes

- Investment option — default "balanced" vs growth vs high-growth

- Insurance inside super — life, TPD, income protection (often opt-out if duplicated elsewhere)

- Fees — admin fees and investment management costs compound over 30 years

Consolidating duplicate accounts reduces fee drag. Check for lost super via ATO online services before rolling funds.

Employer SG vs Salary Sacrifice vs Voluntary Contributions

| Type | Tax treatment | Who pays |

|---|---|---|

| Super Guarantee (SG) | 11.5% employer contribution | Employer |

| Salary sacrifice | Pre-tax from salary; 15% contributions tax in fund | You |

| After-tax voluntary | No contributions tax; may claim tax deduction | You |

Salary sacrifice reduces taxable income now — valuable above $45,000 when marginal rates climb. Contributions tax inside super is 15%, often below your marginal rate.

Concessional cap — $30,000 per year total (SG + salary sacrifice + deductible personal contributions). Excess triggers extra tax.

Model long-term growth with our retirement savings calculator and compound interest calculator.

Investment Options Inside Super

Most funds offer pre-mixed options (conservative, balanced, growth) and sometimes direct ASX/ETF choice. Younger workers with 20+ years to retirement often tolerate higher growth allocations — but only if they will not panic-sell in a 30% downturn.

Review allocation yearly, not daily. Rebalance if your growth sleeve drifts more than 5–10 percentage points from target.

First Home Super Saver (FHSS) Scheme

Eligible Australians can make voluntary contributions and later withdraw up to $50,000 (plus earnings) for a first home deposit. Rules are strict — amounts, timing, and tax on withdrawal. Treat FHSS as a structured savings lane, not a substitute for emergency cash.

Fees, Insurance, and Performance

Low fees matter enormously. A 1% extra fee on $200,000 over 25 years can cost tens of thousands. Compare your fund's net returns after fees against similar options on the APRA heatmap or independent research.

Disable duplicate insurance if you have adequate cover outside super — premiums eat balance silently.

EOFY Planning (30 June)

Before financial year-end:

- Check concessional cap room for salary sacrifice top-ups

- Consider spouse contributions if one partner earns under $40,000 (tax offset may apply)

- Review beneficiary nominations — binding vs non-binding

Pair super strategy with everyday cash flow via our budget calculator.

Super Is One Piece of the Puzzle

Super complements — not replaces — an emergency fund, mortgage strategy, and non-super investments. Keep three to six months of expenses liquid using our emergency fund calculator before maximising voluntary super if cash flow is tight.

Australian super is boring by design: employer money in, low-cost diversified growth, decades of compounding, tax-advantaged contributions when it makes sense. Check your fund once a year, consolidate duplicates, and let time work.

Topics covered

- superannuation

- Australia super

- retirement Australia

- salary sacrifice

Frequently Asked Questions

How much super must my employer pay in Australia?

The Superannuation Guarantee rate is 11.5% of ordinary time earnings in 2024–25, rising gradually to 12%. It is paid on top of salary for eligible employees.

What is salary sacrifice into super?

You redirect part of pre-tax salary into super, reducing taxable income now. Contributions are generally taxed at 15% inside the fund, which is often below marginal income tax rates.

Can I access super before retirement?

Generally no, except under severe financial hardship, compassionate grounds, or specific schemes like First Home Super Saver. Treat super as long-term locked savings.

Should I consolidate multiple super accounts?

Usually yes — duplicate accounts mean duplicate fees and insurance premiums. Check for lost super and compare fund performance and fees before rolling over.