KiwiSaver Explained: New Zealand's Retirement Savings Scheme

Employer contributions, member rates, fund types, and first-home withdrawal rules — how KiwiSaver fits into a New Zealand household budget.

What KiwiSaver Is

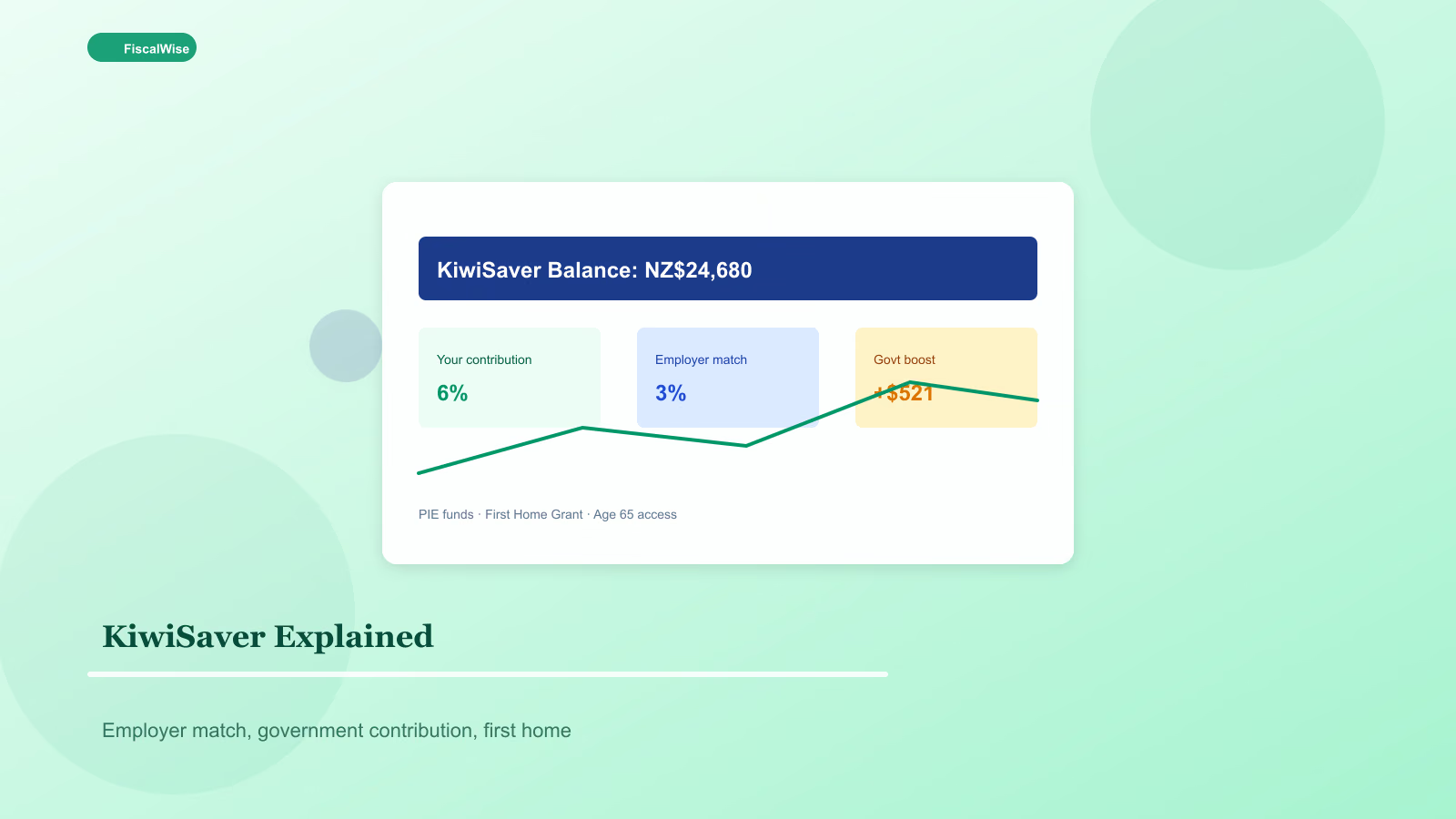

KiwiSaver is New Zealand's voluntary (but auto-enrolled) workplace retirement savings scheme. If you are enrolled, a percentage of gross pay goes to a KiwiSaver provider you choose, and your employer matches at least 3% of gross pay (unless they opt into higher matching).

You can access funds at eligibility age (currently 65) for retirement, or earlier for a first home purchase under strict rules. It is not a government guarantee — balances rise and fall with fund investments.

Contribution Rates

Members choose a contribution rate — typically 3%, 4%, 6%, 8%, or 10% of gross salary. Employers must contribute at least 3% on top if you contribute the minimum.

Government contribution — If you contribute at least $1,042.86 per year (roughly $20/week) and are aged 18–65, the government may add up to $521.43 annually (50 cents per dollar contributed, capped). Missing this match is leaving free money on the table.

Model monthly cash flow with our budget calculator after increasing your KiwiSaver rate.

Choosing a Fund Type

| Fund type | Risk | Typical use |

|---|---|---|

| Defensive / conservative | Low | Near retirement or low risk tolerance |

| Balanced | Medium | Default for many members |

| Growth / aggressive | High | Young members with 20+ years to retirement |

Most providers offer age-based or lifecycle funds that shift toward bonds as you approach 65. Check fees — a 1% difference on a $50,000 balance over 25 years is substantial.

Project long-term outcomes with our retirement savings calculator and compound interest calculator.

First Home Withdrawal

Eligible members can withdraw most of KiwiSaver (except $1,000) for a first home deposit, plus potentially receive a First Home Grant from Kāinga Ora if income and house price caps are met.

Rules change — verify current eligibility on Housing New Zealand and Inland Revenue sites. Do not drain KiwiSaver for a home without a separate emergency fund; our emergency fund calculator helps size liquid reserves.

PIE Funds and Tax

KiwiSaver funds are usually Portfolio Investment Entities (PIEs). Tax is paid within the fund at your prescribed investor rate (PIR) — 10.5%, 17.5%, or 28% depending on income. Using the wrong PIR means paying too much tax or facing a bill later. Update PIR when salary jumps.

KiwiSaver vs Other NZ Investing

| Account | Access | Tax |

|---|---|---|

| KiwiSaver | Locked until 65 (exceptions) | PIE rates |

| Taxable brokerage | Anytime | FIF rules may apply for foreign shares |

| Term deposits | Fixed term | RWT on interest |

KiwiSaver is the employer-match lane. Taxable investing handles medium-term goals KiwiSaver cannot fund.

Common Mistakes

Staying in default fund for decades — Review allocation every few years.

Contributing 3% only — If cash flow allows, 6–10% accelerates retirement and maximises habit.

Ignoring the government $521 — Contribute enough to capture the full annual match.

First home without emergency buffer — Mortgage plus no cash reserve is fragile in NZ's variable-rate environment. Stress-test payments with our mortgage calculator.

Getting Started or Optimising

- Log into your provider portal — know balance and fund type

- Confirm employer is contributing 3%+

- Set contribution to capture government match minimum

- Increase rate 1% after each pay rise

- Check PIR is correct on Inland Revenue myIR

KiwiSaver is New Zealand's simplest retirement building block: auto-enrol, employer match, government boost, and decades of compounded growth. Pick an appropriate fund, raise contributions steadily, and keep emergency cash outside the scheme.

Topics covered

- KiwiSaver

- New Zealand retirement

- NZ investing

- first home NZ

Frequently Asked Questions

How much must my employer contribute to KiwiSaver?

If you are a KiwiSaver member contributing from your pay, your employer must contribute at least 3% of your gross salary, unless they voluntarily contribute more.

What is the KiwiSaver government contribution?

If you contribute at least $1,042.86 per year and are aged 18–65, the government may add up to $521.43 annually — 50 cents for every dollar you contribute, up to the cap.

Can I use KiwiSaver for a first home?

Eligible members can withdraw most of their KiwiSaver balance (except $1,000) for a first home deposit. A First Home Grant may also be available if income and price caps are met.

What KiwiSaver contribution rate should I choose?

Contribute at least enough to get the full government match. If cash flow allows, 6–10% accelerates retirement savings. Increase your rate gradually after pay rises.