Asset Allocation by Age: How to Balance Stocks and Bonds Over Time

Age-based allocation rules, glide paths, and why your sleep-at-night ratio matters more than textbook percentages.

What Asset Allocation Controls

Asset allocation is how you split investments among stocks, bonds, cash, and other assets. It drives more of your portfolio's risk and return than individual stock picks. A 90% stock portfolio can drop 35% in a bad year; a 50/50 mix typically falls less but recovers slower.

Your allocation should match time horizon, goals, and stomach for drawdowns — not your colleague's Twitter portfolio.

Classic Rules of Thumb

| Rule | Stocks % | Bonds % |

|---|---|---|

| --- | ---: | ---: |

| 100 minus age | 100 − age | age |

| 110 minus age (longer lives) | 110 − age | age − 10 |

| 120 minus age (aggressive) | 120 − age | age − 20 |

A 35-year-old under "110 minus age" holds ~75% stocks, 25% bonds. These are starting points, not laws. A 35-year-old saving for a house in three years should not have that down payment in 75% stocks.

Lifecycle Glide Paths

Target-date funds automate allocation — start equity-heavy, shift toward bonds as retirement approaches. Convenient in 401(k)s; less control, but stops emotional drift.

Self-directed investors can glide manually:

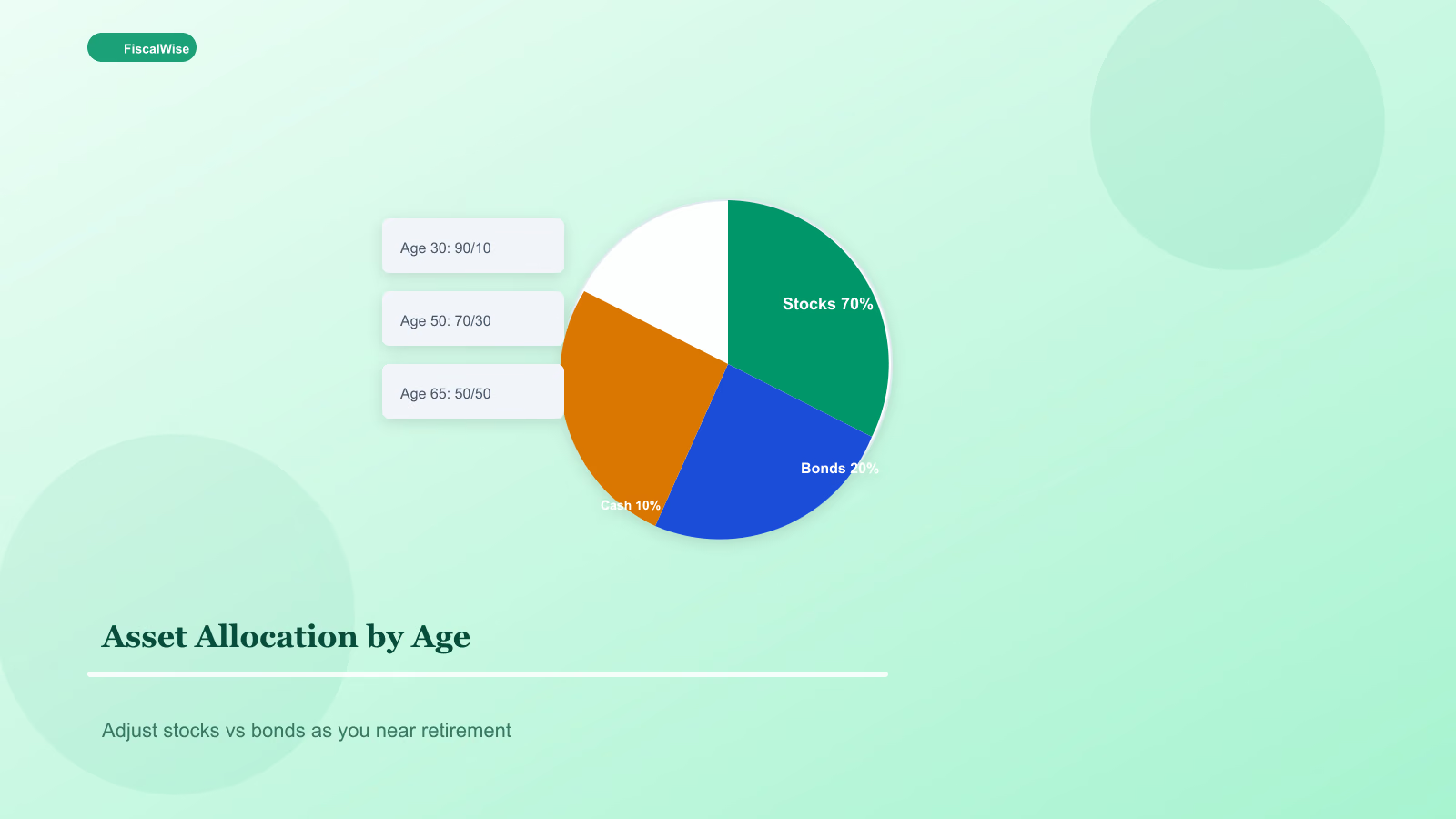

- 20s–30s: 80–90% stocks if retirement is 30+ years out

- 40s: 70–80% stocks; add bonds if volatility causes panic selling

- 50s: 60–70% stocks; build cash bridge for first retirement years

- 60s+: 40–60% stocks depending on spending needs and pensions

Beyond Stocks and Bonds

Modern portfolios may include:

- International equities — 20–40% of stock sleeve

- REITs — inflation-linked income, volatile

- Cash / T-bills — near-term spending, emergency overflow

- Alternatives — optional satellite, not core for beginners

Use our investment return calculator to compare sleeve performance over your actual holding period — not cherry-picked bull years.

Rebalancing: When and How

Markets move; 80/20 becomes 88/12 after a stock rally. Rebalancing sells high, buys low — in theory. In practice:

- Calendar — once or twice yearly

- Threshold — when any sleeve drifts 5+ percentage points

- Cash flow — direct new contributions to underweight sleeve

Avoid rebalancing in taxable accounts if it triggers large gains — redirect contributions instead.

Allocation and Retirement Projections

Stock-heavy early careers maximize expected growth. Our retirement savings calculator shows how extra bond allocation lowers volatility and expected median outcome — tradeoff is feature, not bug.

Pair with net worth calculator reviews yearly: are investment balances growing with plan, or is new debt offsetting market gains?

When Textbook Allocation Fails

Single income, unstable job — Hold larger emergency fund; do not compensate by cutting bonds to 0% unless horizon is 20+ years.

Large guaranteed pension — Acts like bond income; you may hold more stocks in investable portfolio.

Early retirement (FIRE) — Sequence-of-returns risk near retirement date may warrant higher cash bucket — two to three years expenses — even if age says 90% stocks.

Sample Portfolios by Profile

Aggressive 30-year-old: 70% US total market, 20% international, 10% bonds

Moderate 45-year-old: 50% US, 20% international, 25% bonds, 5% REIT

Conservative 58-year-old: 35% US, 15% international, 40% bonds, 10% cash

Adjust to your accounts — all in low-cost index funds or ETFs.

The Sleep Test

If a 30% portfolio drop would make you sell everything, your stock allocation is too high — regardless of age math. Lower stocks until you can stay invested through a bear market. The right allocation is the one you hold in 2008-style headlines.

Asset allocation by age is a map, not GPS. Start with a rule of thumb, adjust for goals and temperament, rebalance yearly, and let decades do the heavy lifting.

Topics covered

- asset allocation

- stocks and bonds

- portfolio

- rebalancing

Frequently Asked Questions

What is the 110 minus age rule?

A common starting point: subtract your age from 110 for stock percentage, remainder in bonds. A 40-year-old might hold 70% stocks and 30% bonds before adjusting for risk tolerance and goals.

How often should I rebalance my portfolio?

Once or twice yearly, or when any asset class drifts five or more percentage points from target. Direct new contributions to underweight sleeves to reduce taxable sales in brokerage accounts.

Should my house down payment be in stocks?

Money needed within five years should not be heavily allocated to equities. Use cash, HYSA, or short-term bonds for near-term goals regardless of your age-based retirement allocation.