Zero-Based Budgeting for Beginners: Give Every Dollar a Job

Learn zero-based budgeting — income minus expenses equals zero — so spending matches priorities instead of drifting month to month.

What Zero-Based Budgeting Actually Means

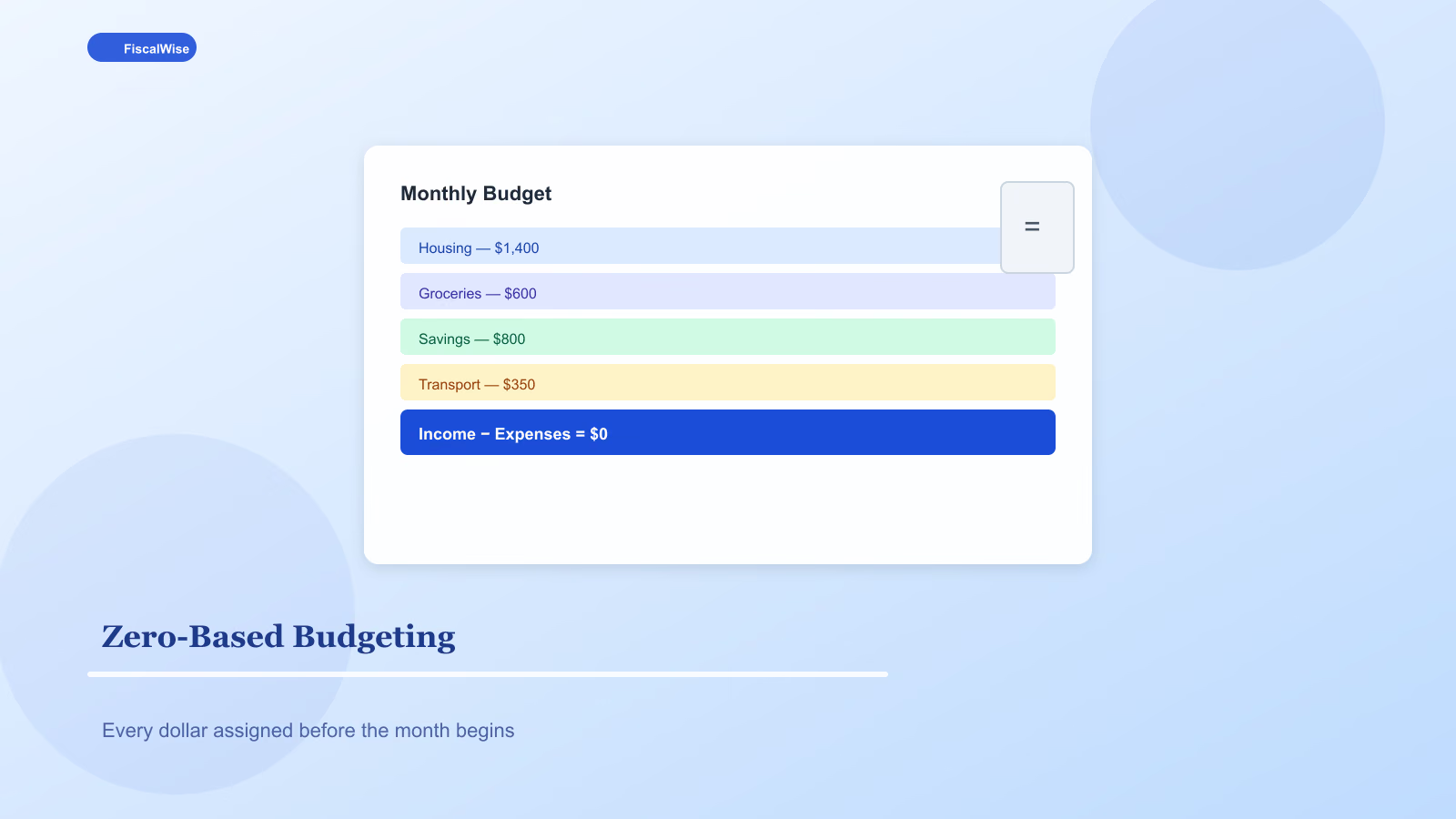

Zero-based budgeting (ZBB) does not mean you have zero dollars left in your bank account. It means every dollar of take-home income is assigned a job before the month starts — rent, groceries, debt payment, retirement, fun money — so income minus planned spending equals zero.

Traditional budgeting often tracks what you already spent. ZBB plans what you will spend. The difference is intention. When $200 sits in "dining out," you can order delivery guilt-free because groceries and savings already got theirs.

Step 1: Know Your Real Take-Home Pay

Start with deposits that actually hit checking, not gross salary. If you are paid biweekly, remember two months a year have three paychecks — decide in advance whether those are bonus savings or cover annual costs.

Use our salary to hourly converter if you mix W-2 income with freelance or hourly side work. Convert everything to monthly equivalents so the budget math stays consistent.

Step 2: List Fixed Expenses First

Fixed costs are the same every month or close enough:

| Category | Examples |

|---|---|

| Housing | Rent, mortgage, HOA |

| Utilities | Electric, gas, water, internet |

| Insurance | Health, auto, renters |

| Debt minimums | Student loans, credit cards, car note |

| Subscriptions | Phone, streaming, software |

These are non-negotiable in the short term. Sum them before allocating a single dollar to restaurants.

Step 3: Estimate Variable Spending Honestly

Groceries, fuel, childcare, and personal care fluctuate. Look at three months of bank statements and use the average — not the best month. Round up slightly. A budget that only works on perfect weeks fails by February.

Step 4: Fund Goals Before Wants

After essentials, assign dollars to:

- Emergency fund contribution

- Retirement (even 3% if that is the start)

- Sinking funds for irregular bills

- Extra debt payments beyond minimums

What remains is discretionary — entertainment, hobbies, gifts. If nothing remains, cut wants or increase income before skipping goals. Skipping retirement for takeout every month trades compound growth for temporary convenience.

Run the numbers through our budget calculator to see surplus or deficit instantly. A negative number means the plan needs adjustment, not that the method failed.

Step 5: Reconcile Weekly

Check actual spending against categories every Sunday. Move money between categories in your app if groceries ran high but dining was low — the month still totals zero, but categories flex.

Cash envelopes still work for overspenders. Physical cash for "fun" ends when the envelope is empty. Digital-only budgets need the same discipline via separate accounts or category caps.

Common Beginner Mistakes

Budgeting gross income — taxes and benefits already took their share.

Forgetting annual costs — divide car registration, Amazon Prime, and holiday gifts by 12 and fund monthly sinking lines.

No fun line — restrictive budgets snap. A small "guilt-free" category prevents binge spending.

Giving up after one bad month — ZBB is a monthly reset, not a pass/fail test.

Zero-Based vs. 50/30/20

The 50/30/20 rule (needs/wants/savings) is a starting template. ZBB is the detailed implementation. Many people use 50/30/20 to sanity-check proportions, then ZBB to assign actual dollars.

| Method | Best for |

|---|---|

| 50/30/20 | Quick structure, first-time budgeters |

| Zero-based | Detail-oriented households, irregular income |

| Pay-yourself-first | Aggressive savers who automate then spend the rest |

Make Month Two Easier

Copy last month's template. Adjust categories that were consistently over or under. Within three months, most people need only small tweaks.

Zero-based budgeting is paperwork upfront and freedom all month. Every dollar with a name is a dollar that cannot leak unnoticed into subscriptions and delivery fees you stopped enjoying months ago.

Topics covered

- zero-based budget

- budgeting

- monthly budget

- money management

Frequently Asked Questions

What does zero-based budgeting mean?

Every dollar of take-home income is assigned a category before the month starts so income minus planned spending equals zero. It does not mean spending every dollar — savings and debt payments are assigned jobs too.

How is zero-based budgeting different from 50/30/20?

50/30/20 is a rough split between needs, wants, and savings. Zero-based budgeting assigns specific dollar amounts to each line item. Many people use 50/30/20 to check proportions, then ZBB for monthly detail.

How often should I update a zero-based budget?

Create a new plan at the start of each month and reconcile actual spending weekly. Copy last month's template and adjust categories that were consistently over or under budget.

What if my expenses exceed my income on paper?

The budget is telling you the plan is unsustainable. Trim discretionary spending, renegotiate fixed bills, or increase income before the month starts — not after overdraft fees hit.