Living Paycheck to Paycheck? How to Break the Cycle

Concrete steps to build breathing room when every month starts at zero — without pretending a latte is the whole problem.

Paycheck to Paycheck Is a Cash-Flow Problem, Not a Character Flaw

Roughly half of Americans live paycheck to paycheck at some point — including households with six-figure incomes in high-cost cities. The pattern is simple: money in, money out, little or no buffer before the next deposit. One missed shift or surprise bill triggers overdraft fees, credit card float, or borrowed money from family.

Breaking the cycle requires separating three levers: what you earn, what you must pay, and what leaks without notice. Moralizing about coffee ignores rent that consumes 45% of take-home pay. Start with math, not shame.

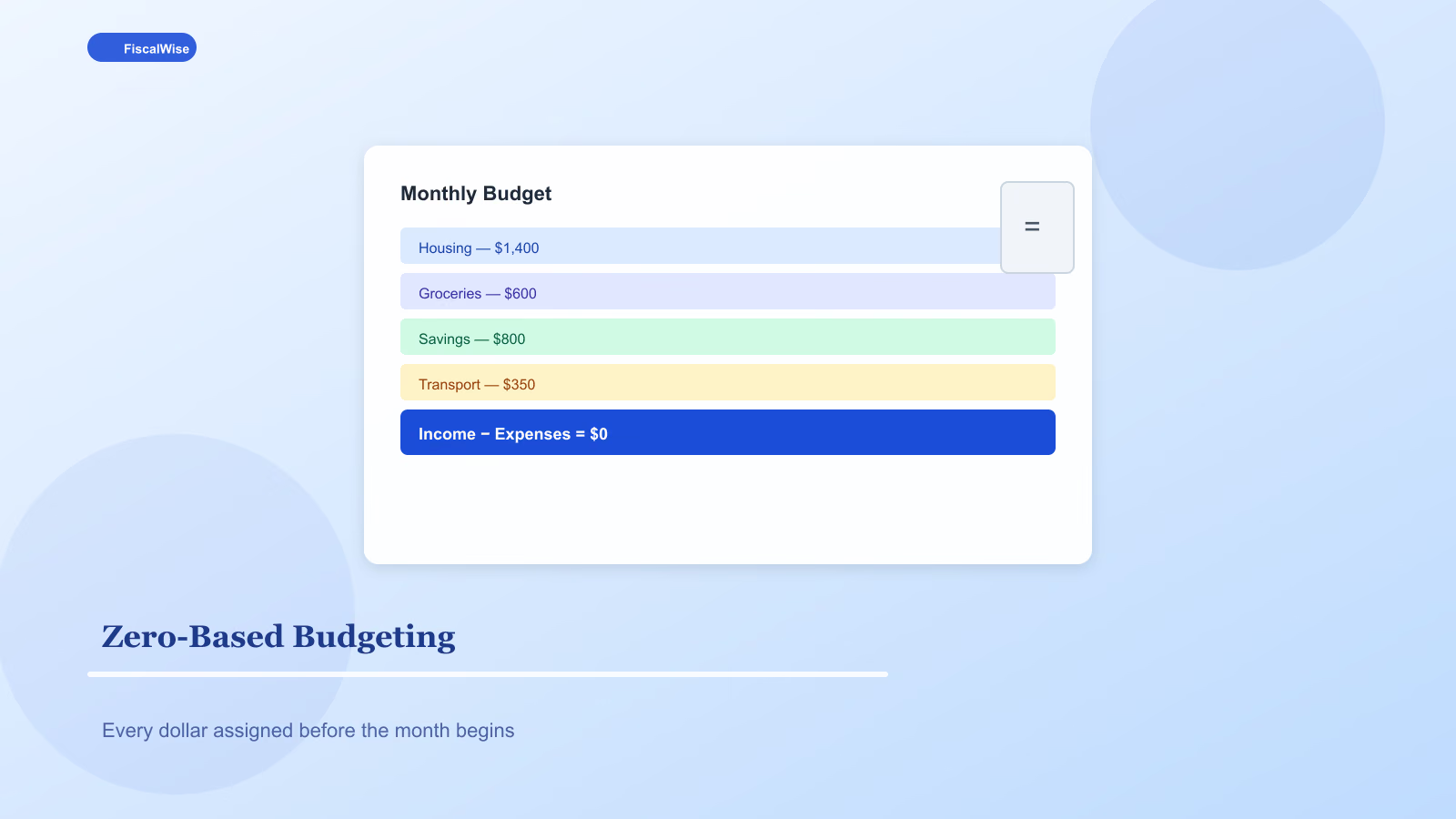

Map One Month of Truth

Export 30–60 days of checking and card transactions. Tag each line:

- Fixed must-pay — housing, utilities, insurance, minimum debt

- Variable essential — food, transport, medicine

- Discretionary — dining, entertainment, shopping

- Leakage — subscriptions, fees, impulse buys, buy-now-pay-later

Our budget calculator helps total categories. You are looking for the gap between income and must-pay plus essentials. If that gap is negative, no amount of coupon clipping fixes it — income or housing cost must change.

Find $100 Before You Hunt $1,000

Small wins build momentum:

- Pause one subscription tier downgrade

- Switch phone plan at renewal

- Move insurance deductibles only if emergency fund can cover them

- Meal-plan three dinners weekly

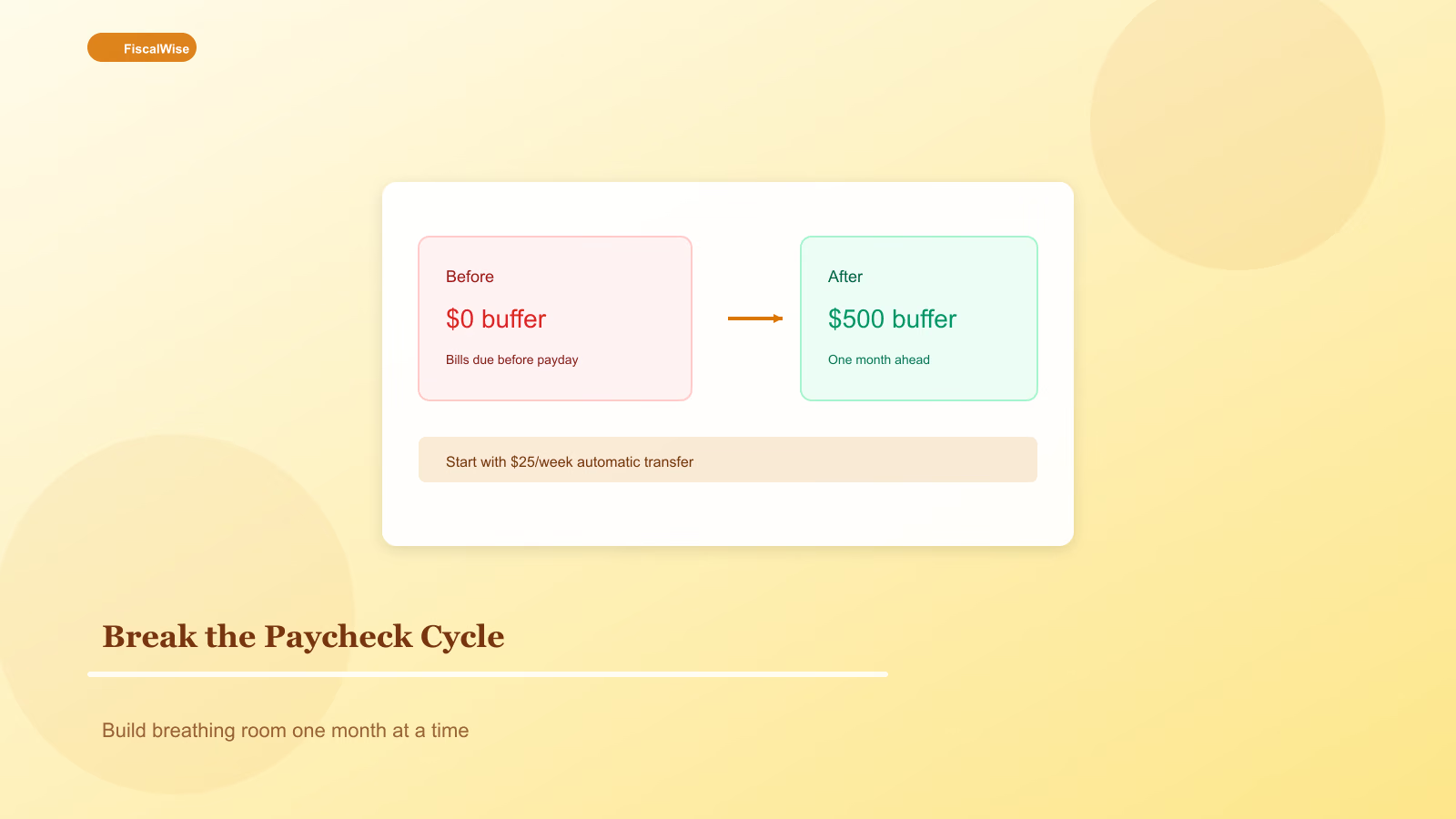

Automate $25–$50 per paycheck to a separate savings account before other spending. Name it "buffer." The goal is one week's essentials, then two, then a full month.

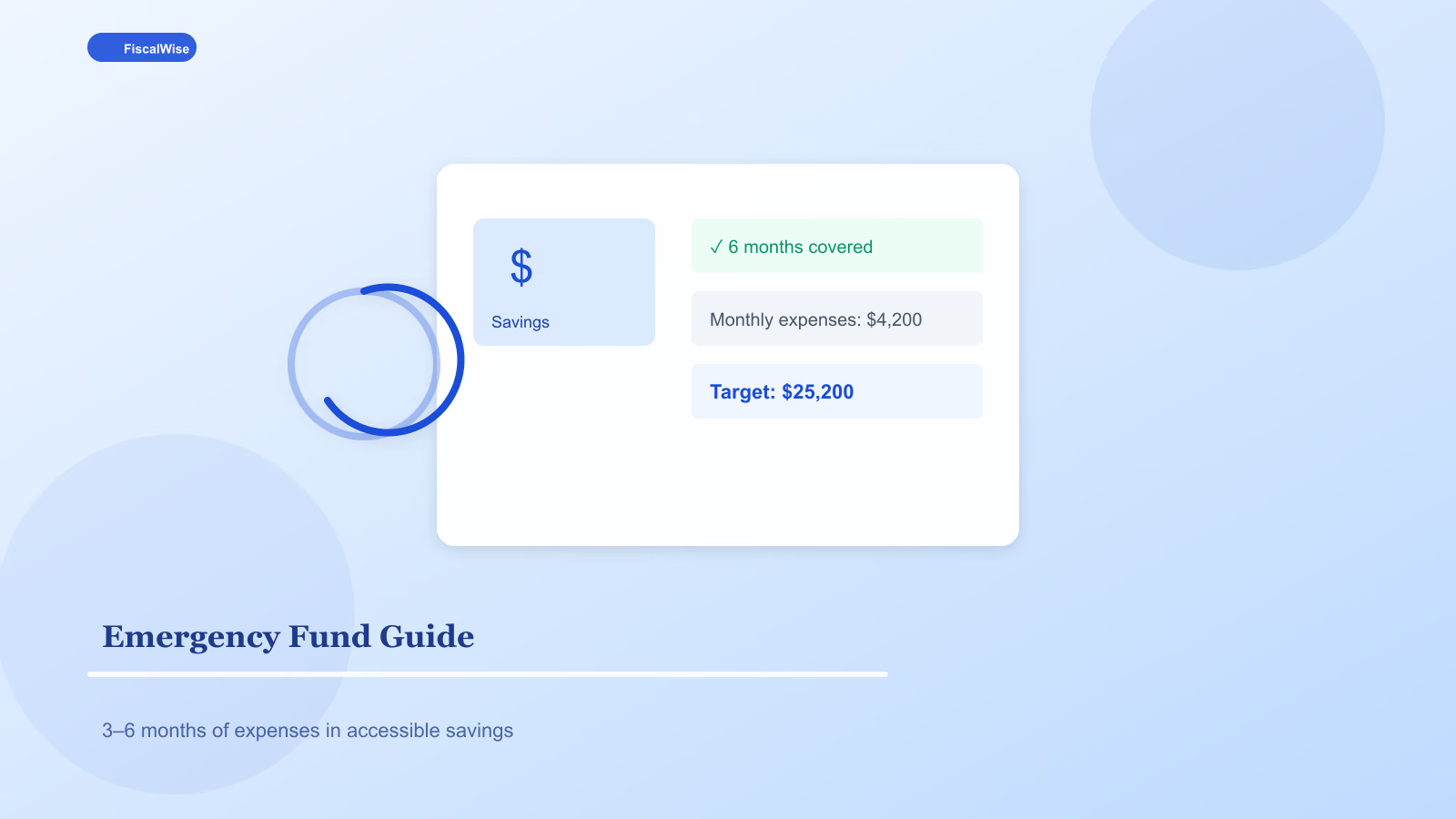

Track progress with the emergency fund calculator. One month of essentials in cash changes psychology even before you hit the full three-to-six-month target.

Attack Expensive Debt First

Minimum payments on high-APR cards consume cash flow without shrinking principal fast. List every balance and rate. Even $50 extra on the highest APR card saves hundreds in interest and frees payment room sooner.

Our debt payoff calculator compares snowball and avalanche timelines. Pick the method you will stick with — avalanche saves more interest; snowball wins on early victories.

Increase Income Without a Fantasy Side Hustle

Sustainable income boosts:

- Overtime or on-call shifts if available

- Sell skills you already have — tutoring, bookkeeping, design

- Ask for a raise with documented contributions, not vibes

- Temporary second job with a defined end date

Convert job offers and freelance quotes with the salary to hourly converter so part-time hours are worth the commute and tax hit.

Timing Fixes That Cost Nothing

If bills cluster in week one and pay arrives week two, call providers. Many utilities and lenders adjust due dates once per year. Spreading due dates across the month prevents artificial crises.

Biweekly earners get two "extra" paychecks yearly. Mark them on the calendar now — assign to emergency fund or annual bills, not lifestyle inflation.

When Cutting Is Not Enough

If essentials exceed income after honest review:

- Housing swap — roommate, smaller unit, different neighborhood

- Transportation — sell car payment for reliable used + cash purchase when possible

- Benefits — ACA marketplace, employer HSA, local assistance programs

These are hard choices. Staying paycheck to paycheck with no plan is harder over years.

Build Systems, Not Willpower

- Autopay fixed bills on payday

- Separate accounts: bills, spending, savings

- Weekly 15-minute money check-in

- No new BNPL while digging out

Breaking the paycheck cycle is slow until it is sudden — one month you cover an insurance deductible without panic, then you forget how that used to feel impossible. That is the win.

Topics covered

- paycheck to paycheck

- cash flow

- budgeting

- financial stress

Frequently Asked Questions

How long does it take to break the paycheck-to-paycheck cycle?

Most households need three to twelve months to build one month's essential expenses in buffer savings, depending on income gap and spending cuts. Full emergency funds take longer — progress accelerates once high-APR debt stops growing.

Can I break the cycle without earning more money?

Sometimes, if the gap between income and essentials is positive but leaks consume the surplus. If essentials exceed income after honest review, income or housing cost must change — cutting alone is not enough.

What is the first step if I overdraft every month?

Map one month of transactions into fixed, essential, discretionary, and leakage categories. Automate a small transfer to a separate buffer account on payday — even $25 — before discretionary spending.

Should I use buy-now-pay-later while building savings?

Pause BNPL and new credit while building buffer savings. Installment plans fragment cash flow and make true spending invisible until payments cluster.