High-Yield Savings Accounts: Where to Park Your Cash in 2026

Compare HYSA rates, FDIC protection, and when cash belongs in savings versus investing — without chasing teaser yields.

Why Your Big-Bank Savings Account Pays Almost Nothing

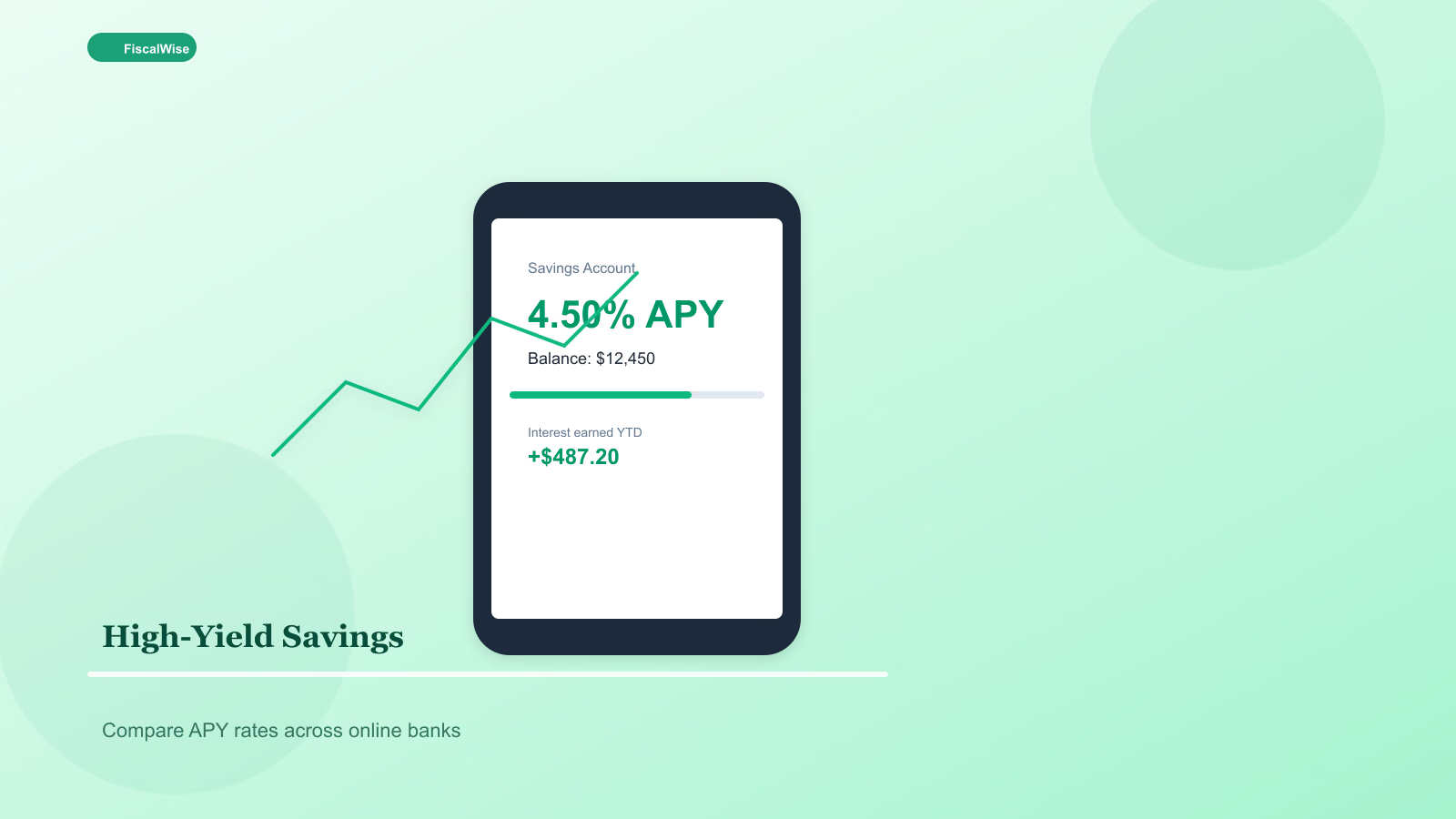

Brick-and-mortar banks often pay 0.01–0.10% on standard savings while lending those deposits at much higher rates. High-yield savings accounts (HYSAs) — mostly online banks and fintechs — pass more of that spread to you. In 2026, competitive HYSAs still offer meaningfully more than traditional accounts, though rates fluctuate with Federal Reserve policy.

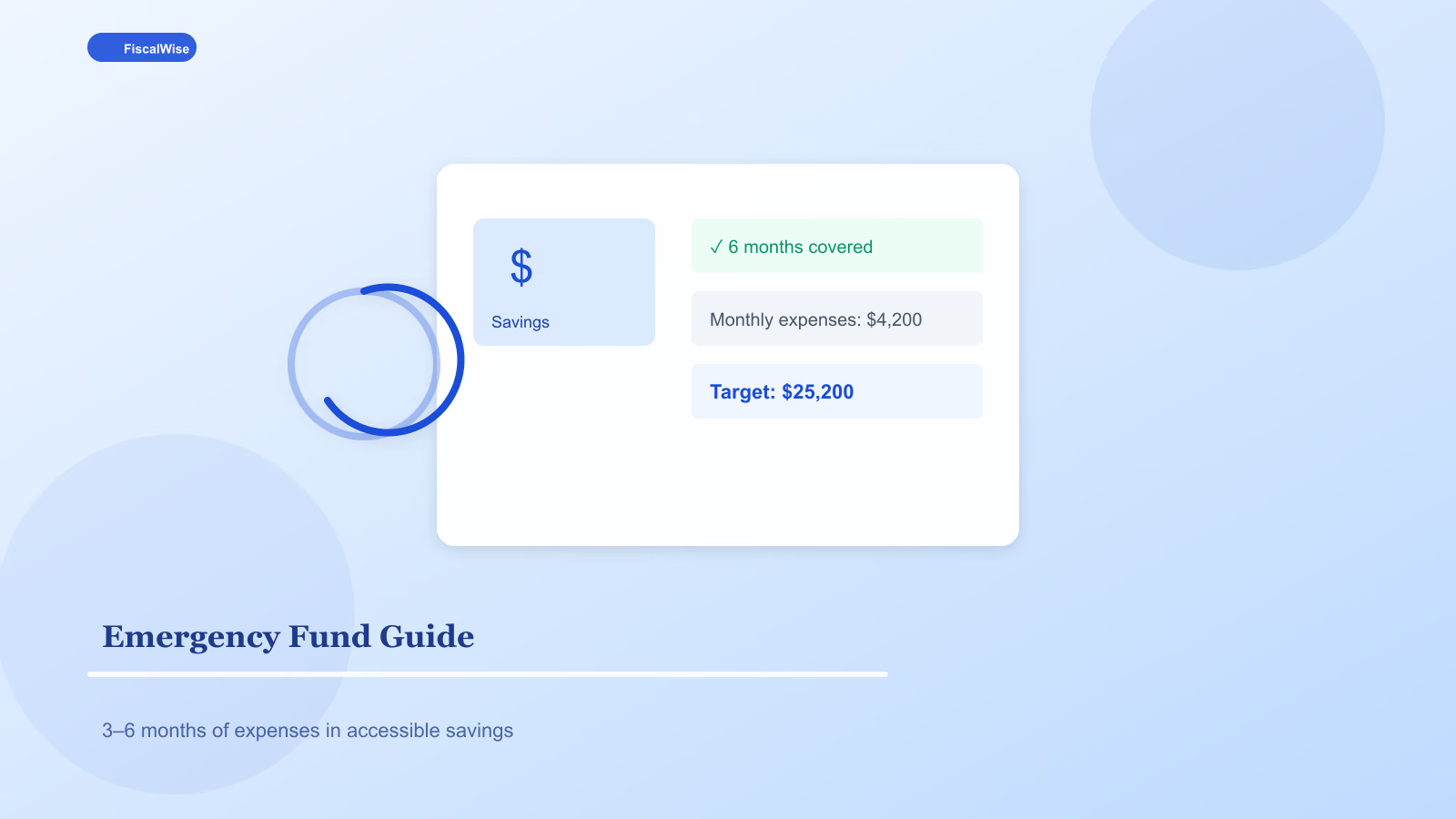

On a $10,000 emergency fund, the difference between 0.05% and 4.50% is roughly $445 per year. That is not life-changing wealth, but it is free money for money you need liquid anyway.

What to Look for Beyond the Headline Rate

FDIC or NCUA insurance — Confirm the institution is federally insured up to $250,000 per depositor, per bank. Credit unions use NCUA; coverage is equivalent for consumers.

No monthly fees — Legitimate HYSAs rarely charge maintenance fees. Walk away from accounts that do.

Transfer speed — Can you move money to checking in one business day? Emergency funds need access, not a five-day hold.

Rate history, not just teaser APY — Some banks spike rates to attract deposits then cut. Read reviews and check whether the rate has been stable for quarters, not weeks.

Mobile experience — If you cannot see balances and initiate transfers easily, you will underuse the account.

HYSA vs. Money Market vs. CDs

| Product | Liquidity | Typical use |

|---|---|---|

| HYSA | Immediate to 1 day | Emergency fund, short goals |

| Money market account | Similar to HYSA | Often higher minimums |

| CD | Locked for term | Known expense 6–18 months out |

Certificates of deposit pay a fixed rate but penalize early withdrawal. Do not lock emergency cash in a 12-month CD. Do use CDs for expenses with a fixed date — next year's tuition installment, property tax if you lack escrow discipline.

How Interest Compounds

HYSAs compound daily or monthly. Over years, compounding matters. Model growth with our compound interest calculator: $500 monthly at 4.5% for five years lands near $33,500 from $30,000 contributed — modest but real.

Remember inflation erodes purchasing power. A inflation calculator shows why long-term wealth belongs in diversified investments, not cash forever. The HYSA's job is safety and liquidity, not retirement growth.

How Much Should Sit in Cash?

Rules of thumb:

- Emergency fund — 3–6 months essentials in HYSA

- Near-term goals — Down payment within 2 years, wedding next year — HYSA or short CDs

- Everything else — Invest per your risk tolerance and timeline

If your emergency fund is full and short-term goals are funded, excess cash is a drag. Move incremental savings toward retirement or taxable investing.

Opening and Organizing Multiple Accounts

Some people use one HYSA for emergencies and another for sinking funds, labeled in a spreadsheet. Others use one account with a ledger. Separation reduces accidental spending; consolidation reduces rate-chasing admin.

When rates diverge widely, moving emergency cash to a better HYSA is reasonable. Do not churn monthly — the tax on your time adds up.

Tax on Savings Interest

Interest is ordinary income. Banks send Form 1099-INT if you earned $10 or more. Plan for a small tax bill in April if you keep large balances at high rates.

The Bottom Line

A high-yield savings account will not make you rich. It will keep your emergency fund and short-term goals earning something while staying safe and accessible. Pair the right HYSA with clear goals in our savings goal calculator and you stop leaving hundreds on the table every year.

Topics covered

- high-yield savings

- HYSA

- savings account

- interest rates

Frequently Asked Questions

Are high-yield savings accounts safe?

FDIC-insured HYSAs protect deposits up to $250,000 per depositor per bank. Verify insurance status before opening. Credit union equivalents use NCUA coverage.

How is a HYSA different from a money market account?

Both offer liquidity and interest. Money market accounts sometimes include check-writing and higher minimums. For emergency funds, either works if FDIC-insured and fee-free.

Should I keep all my savings in a HYSA?

Keep emergency funds and short-term goals in HYSA. Long-term wealth belongs in diversified investments — cash loses purchasing power to inflation over decades.