How to Build an Emergency Fund: A Step-by-Step Guide

A practical roadmap to fund three to six months of essential expenses — even when money feels tight and surprises keep showing up.

Why an Emergency Fund Comes Before Everything Else

An emergency fund is cash you can reach in days, not weeks. It covers the furnace that dies in January, the deductible after a fender bender, or three months of rent if your industry has a rough quarter. Without it, every surprise becomes a credit card balance at 22% APR — and that spiral is harder to unwind than the original problem.

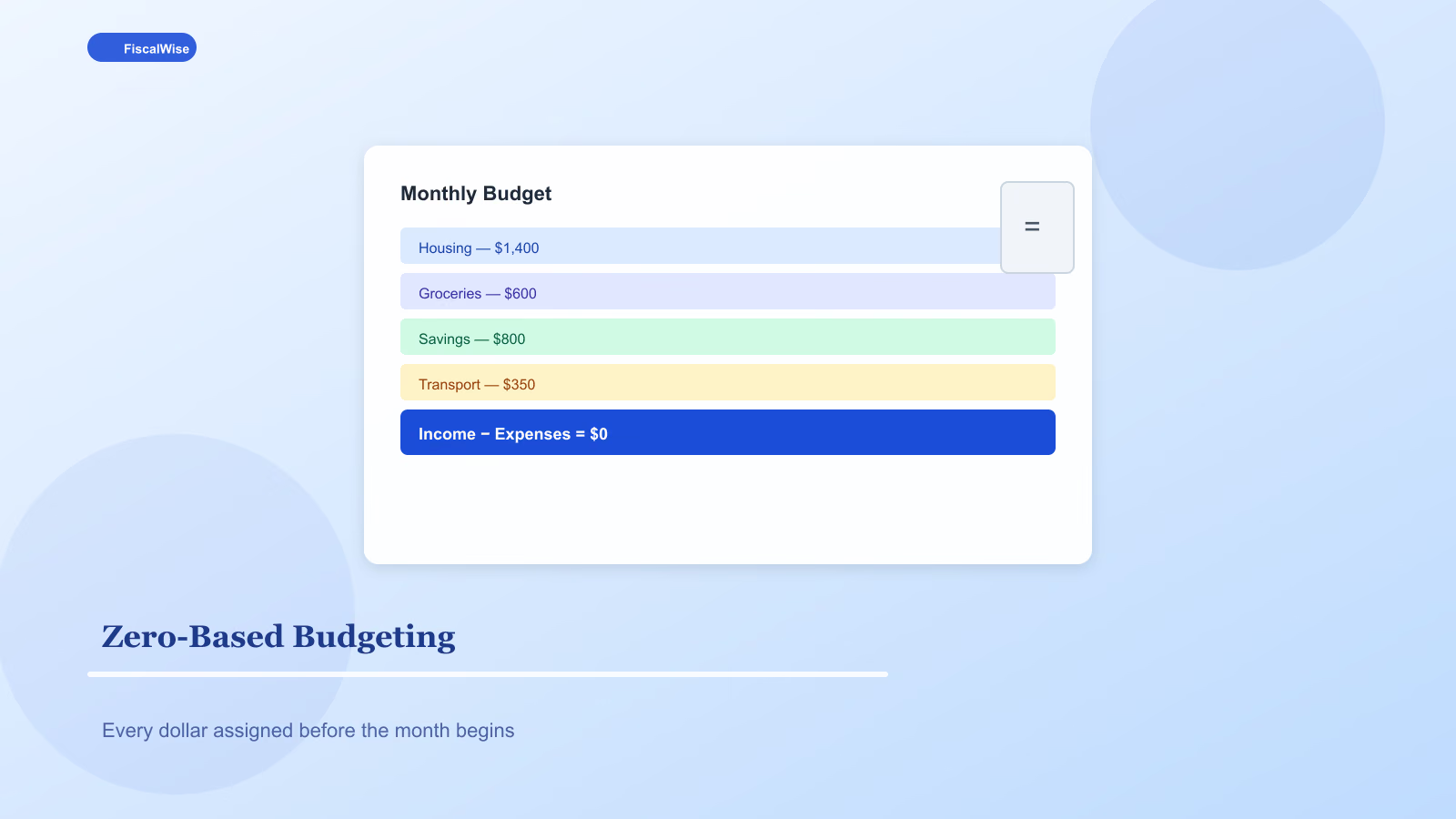

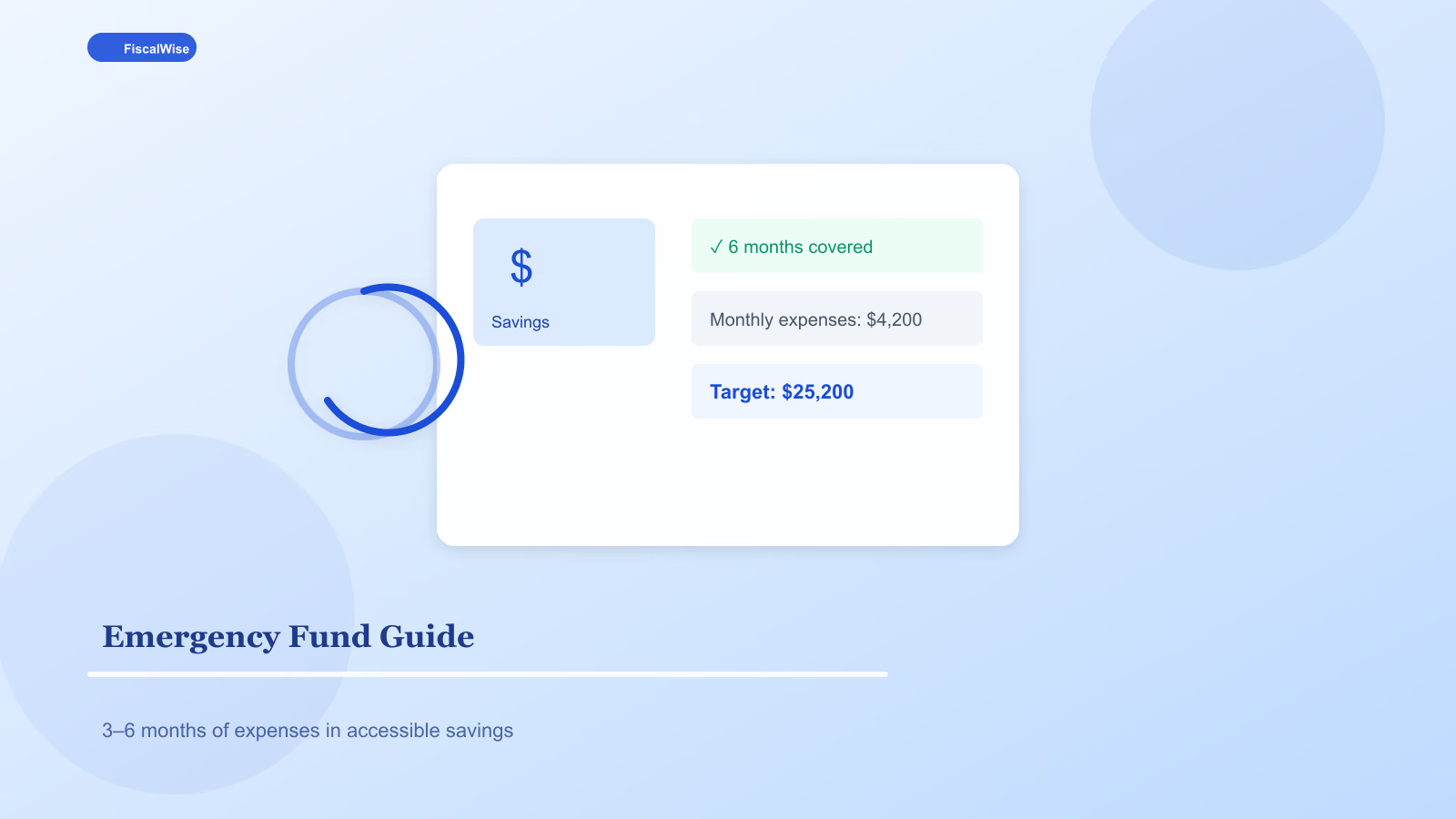

The goal is not a vague "save more." It is a specific number tied to your essential monthly spending. Most households target three to six months of bare-bones expenses. Three months works when you have stable W-2 income and a partner who can cover gaps. Six months makes sense for freelancers, commission earners, single-income families, or anyone in a volatile sector.

Use our emergency fund calculator to turn your rent, utilities, groceries, insurance, and minimum debt payments into a concrete target. If essentials run $3,200 a month, a four-month fund is $12,800. That number might sting — but it is honest.

Start With $1,000, Then Build the Full Cushion

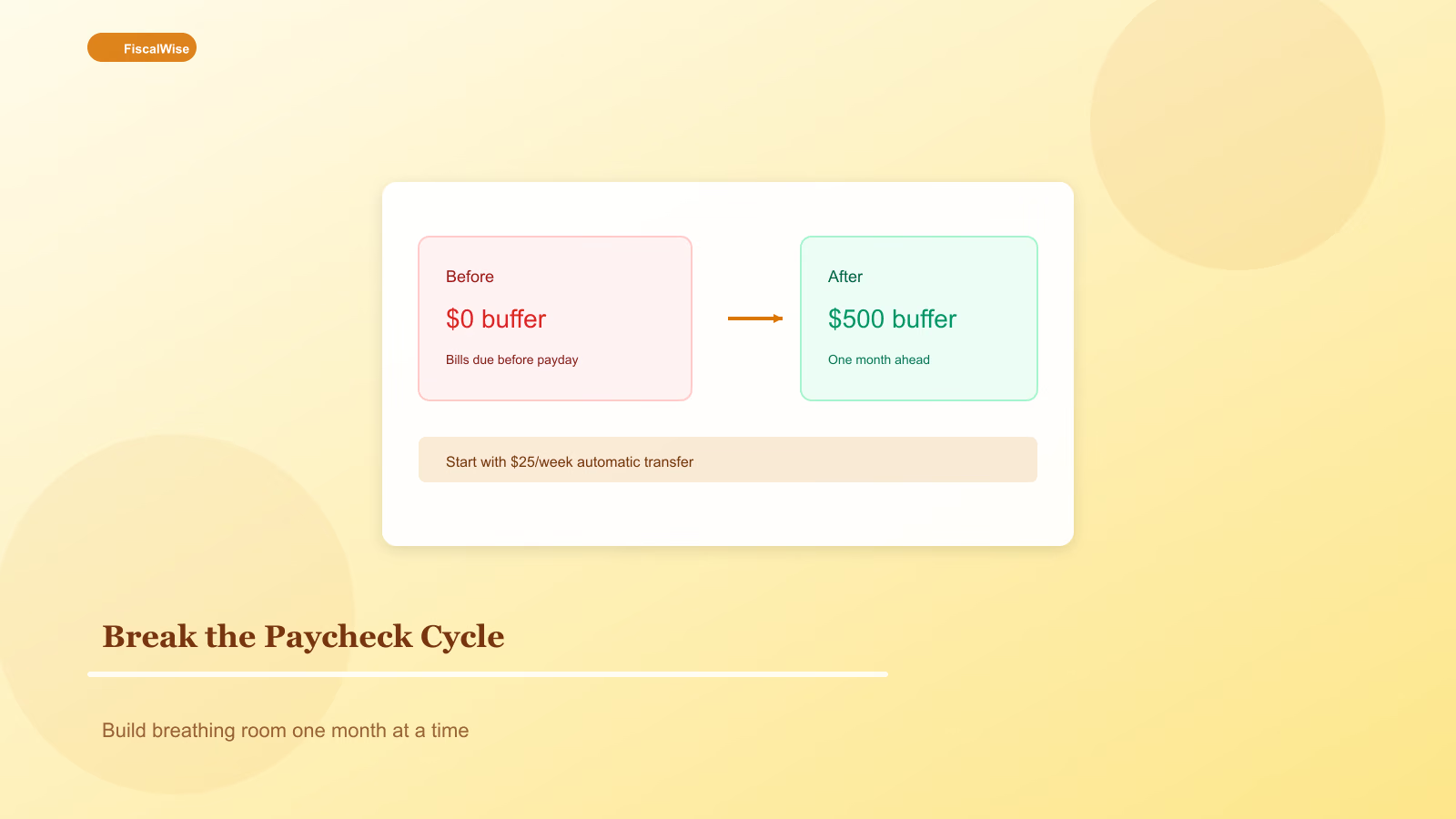

Dave Ramsey's $1,000 starter fund gets mocked online, but the psychology is sound: something in the bank changes how you react to a flat tire. Park $1,000 in a separate high-yield savings account before you attack credit card debt aggressively. Then refill and scale toward your full target.

If $1,000 feels impossible, start with $500. Automate $25 every payday. The habit matters more than the opening balance. Savings that require a decision every month rarely survive a busy Tuesday.

Where to Keep Emergency Cash

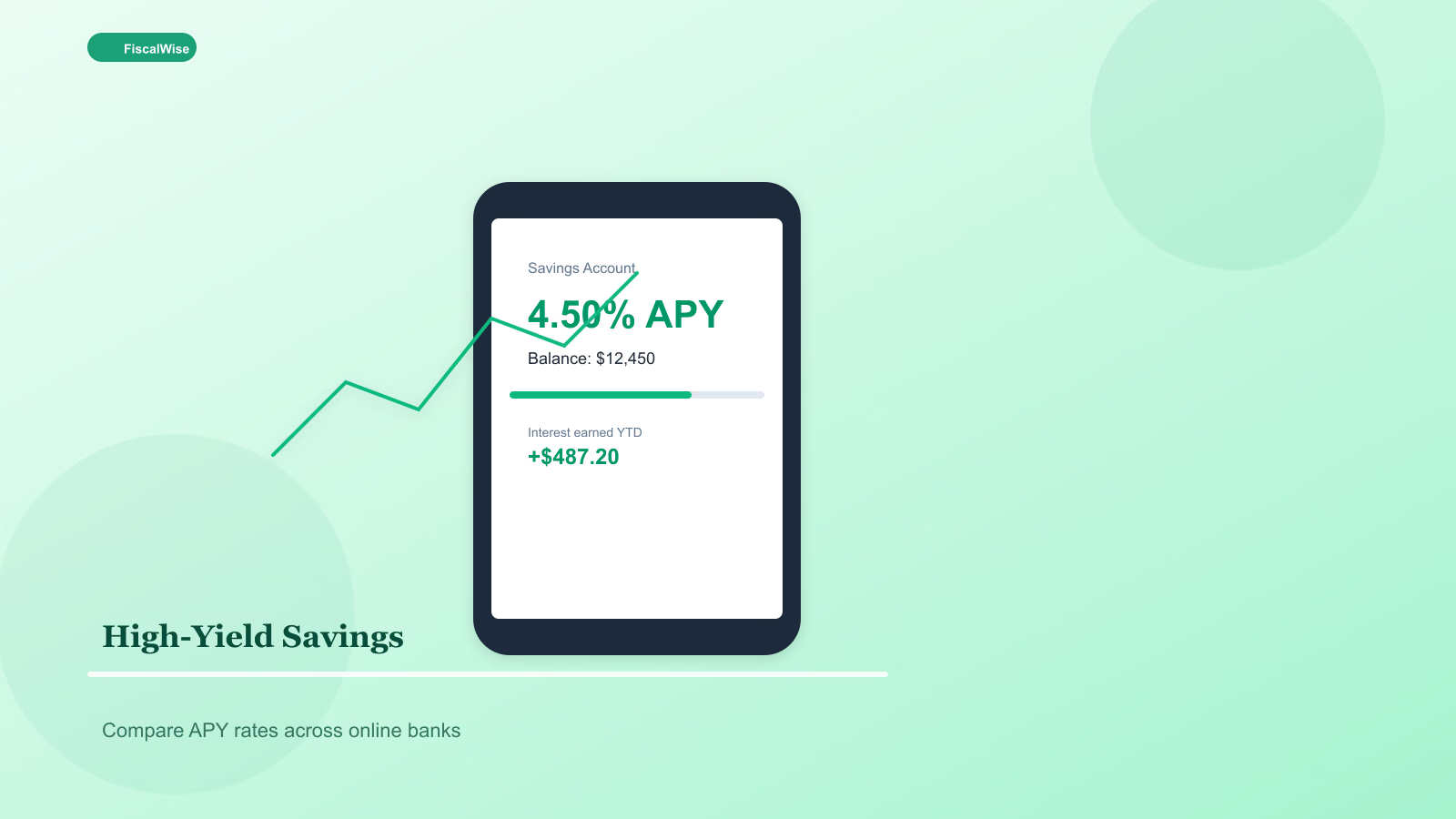

Emergency money belongs in an FDIC-insured savings account or equivalent — not stocks, not crypto, not a six-month CD you cannot break without penalty. You are buying liquidity and sleep, not maximum return.

High-yield online savings accounts often pay 4–5% while keeping same-day or next-day transfers to checking. Label the account "Emergency — do not touch" in your banking app. Out of sight helps; out of the spending account helps more.

How to Fund It Without a Second Job

Automate first. Schedule a transfer on payday before you browse takeout apps. Even $50 per check adds $1,300 a year on biweekly pay.

Redirect one windfall. Tax refund, bonus, or side-gig month — send 50–100% to the fund once, then return to normal contributions.

Trim one recurring leak. Cancel a subscription you forgot about, negotiate insurance at renewal, or meal-prep two lunches a week. Route the savings directly — not through checking where it disappears.

Sell once. List unused electronics, furniture, or gear one weekend. A $400 declutter jump-starts the account faster than months of $25 transfers.

Pair this with a budget calculator pass so you know exactly how much slack exists after fixed bills. Guessing leads to over-promising and quitting.

What Counts as an Emergency

Emergencies are unexpected, necessary, and urgent. Job loss, medical bills after insurance, emergency travel for family, major car repair so you can commute.

Planned expenses are not emergencies: holidays, annual insurance premiums, property tax, replacing a phone you knew was dying. Those belong in sinking funds — separate labeled savings buckets you fund monthly. Our savings goal calculator works for those targets too.

Inflation and Your Target

A fund sized two years ago may be short today. Essentials creep up — rent, groceries, insurance. Recalculate yearly using an inflation calculator mindset: if costs rose 3% annually, a $12,000 target from 2024 should be closer to $12,700 in 2026.

When to Use It — and When to Refill

If you tap the fund, pause optional spending until you rebuild at least one month's expenses, then resume filling to full target. Treat refill like a bill with a due date. The fund only protects you if it comes back.

Building an emergency fund is boring, visible, and one of the highest-return moves in personal finance — not because of interest earned, but because it keeps you off expensive debt when life does what life does.

Topics covered

- emergency fund

- savings

- financial security

- rainy day fund

Frequently Asked Questions

How much should I have in an emergency fund?

Most households target three to six months of essential expenses — housing, utilities, food, insurance, and minimum debt payments. Stable W-2 earners often start at three months; freelancers and single-income families often aim for six.

Should I pay off debt or build an emergency fund first?

Save a starter fund of $500–$1,000 first so minor surprises do not become new credit card debt. Then balance debt payoff with building toward your full three-to-six-month target.

Where is the best place to keep an emergency fund?

Use an FDIC-insured high-yield savings account with same-day or next-day transfers to checking. Avoid stocks, crypto, or CDs with early-withdrawal penalties for emergency cash.

What counts as a true emergency?

Job loss, urgent medical bills after insurance, essential car repairs, or unexpected travel for family crises. Planned expenses like holidays or annual premiums belong in sinking funds, not emergency savings.