US Federal Tax Brackets Explained: Marginal vs. Effective Rates

How progressive tax brackets work, why a raise rarely doubles your tax bill, and planning moves that use bracket awareness.

Progressive Brackets, Not Flat Tax on Everything

The US federal income tax system is progressive: higher chunks of income face higher rates. Moving into the 24% bracket does not mean all income is taxed at 24% — only dollars above the prior bracket threshold are.

This confusion costs people raises they fear and leads to bad side-gig math ("I'll lose it all to taxes"). Understanding marginal vs. effective rate fixes that.

Marginal vs. Effective Rate

Marginal rate — tax on the next dollar of taxable income. If you are $500 below the 24% bracket, a $1,000 bonus might be partly at 22% and partly at 24%.

Effective rate — total tax ÷ total taxable income. A household with 22% marginal rate often pays 12–15% effective because lower brackets soaked most income first.

Our tax bracket calculator shows both for your filing status and income — use it before major financial moves.

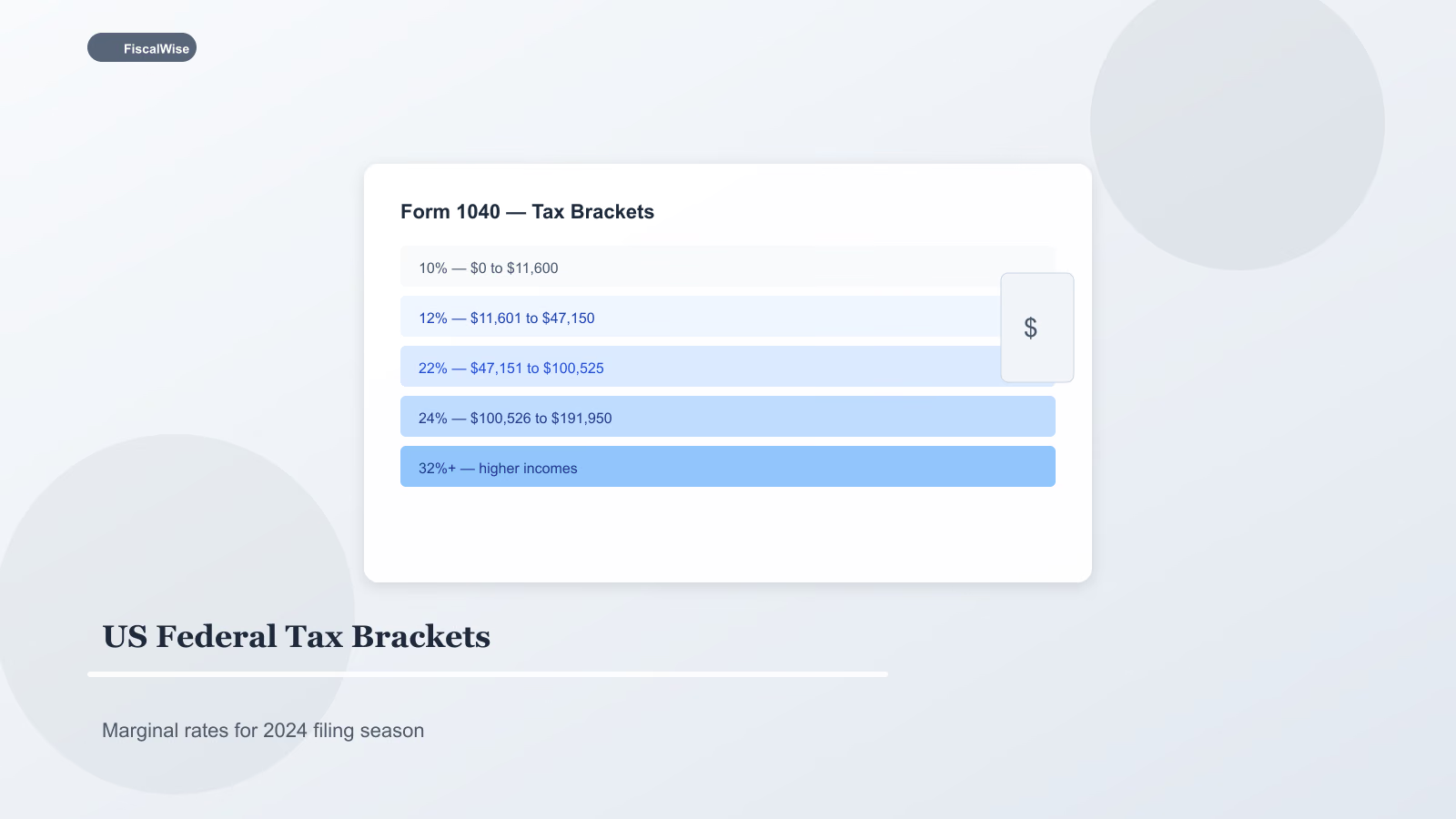

2026 Brackets (Illustrative Structure)

IRS updates thresholds annually for inflation. Structure for married filing jointly typically spans:

| Rate | Taxable income band (example structure) |

|---|---|

| ---: | --- |

| 10% | Lowest band |

| 12% | Next band |

| 22% | Middle earners |

| 24% | Upper middle |

| 32% | High earners |

| 35% | Very high |

| 37% | Top band |

Single filers hit each threshold at lower dollar amounts. Always verify current year tables on IRS.gov or FiscalWise updates.

Taxable Income Starts After Reductions

Gross salary is not bracket input. Subtract:

- Standard deduction (or itemized deductions)

- Pre-tax 401(k), HSA, traditional IRA contributions

- Other above-the-line adjustments where eligible

A $90,000 gross with $24,000 standard deduction and $10,000 401(k) contribution lands near $56,000 taxable — very different bracket picture.

Convert salary offers to monthly take-home with the salary to hourly converter after rough tax estimates for budgeting — not as CPA replacement.

Common Bracket Myths

"Bonus taxed higher" — Bonuses often use withholding tables that feel punitive; true marginal rate on bonus income may be lower than withholding suggests. Reconcile on Form 1040.

"Overtime not worth it" — Almost always worth it unless benefits cliff or income-based repayment plans create rare phaseouts.

"Marriage penalty always" — MFJ shares wider brackets; some couples pay less combined, some more depending on income split.

Planning Moves Using Brackets

Traditional 401(k) / IRA — Dollars that would have been taxed at 22–24% grow tax-deferred; withdraw maybe at 12–22% in retirement if income drops.

Roth conversions in low years — Fill 12% or 22% bucket deliberately when between jobs or early retirement.

Capital gains stacking — Long-term gains brackets are separate; timing sales across tax years can keep 0% or 15% LTCG rates.

Charitable bunches — Donor-advised funds let you itemize one year, standard deduction next.

State and Local Taxes Stack

Federal brackets ignore state income tax — California, New York, New Jersey add meaningful marginal percentages. Plan holistically if you are mobile.

Self-Employed Bracket Reality

Schedule C profit hits income tax brackets plus 15.3% self-employment tax on net earnings (with deduction for employer-equivalent portion). Quarterly estimated payments prevent April surprises.

Year-End Checklist

- Project December taxable income with calculator

- Max retirement accounts if bracket justifies

- Harvest losses if gains pushed you up (see tax-loss harvesting guide)

- Defer or accelerate income if self-employed with bracket visibility

Federal tax brackets are a staircase, not a cliff. Know your next step, plan contributions and conversions around marginal rates, and ignore anyone who says earning more always fails after taxes.

Topics covered

- tax brackets

- federal income tax

- marginal rate

- effective rate

Frequently Asked Questions

What is the difference between marginal and effective tax rate?

Marginal rate is tax on your next dollar of taxable income. Effective rate is total tax divided by total taxable income. A household in the 22% marginal bracket often pays 12–15% effective because lower brackets taxed most income first.

Does a raise push all my income into a higher bracket?

No. Only dollars above each bracket threshold are taxed at the higher rate. Moving into the 24% bracket does not retroactively tax your entire salary at 24%.

How do pre-tax 401(k) contributions affect my bracket?

Traditional 401(k) contributions reduce taxable income, which can keep you in a lower marginal bracket and lower your overall tax bill for the year.

Do tax brackets include state income tax?

Federal brackets ignore state taxes. High-tax states add their own marginal rates on top of federal liability — plan holistically if you are comparing locations or job offers.