Tax-Loss Harvesting Basics: Turn Market Drops Into Tax Savings

How to realize investment losses strategically, offset gains, and navigate wash-sale rules without tripping the IRS.

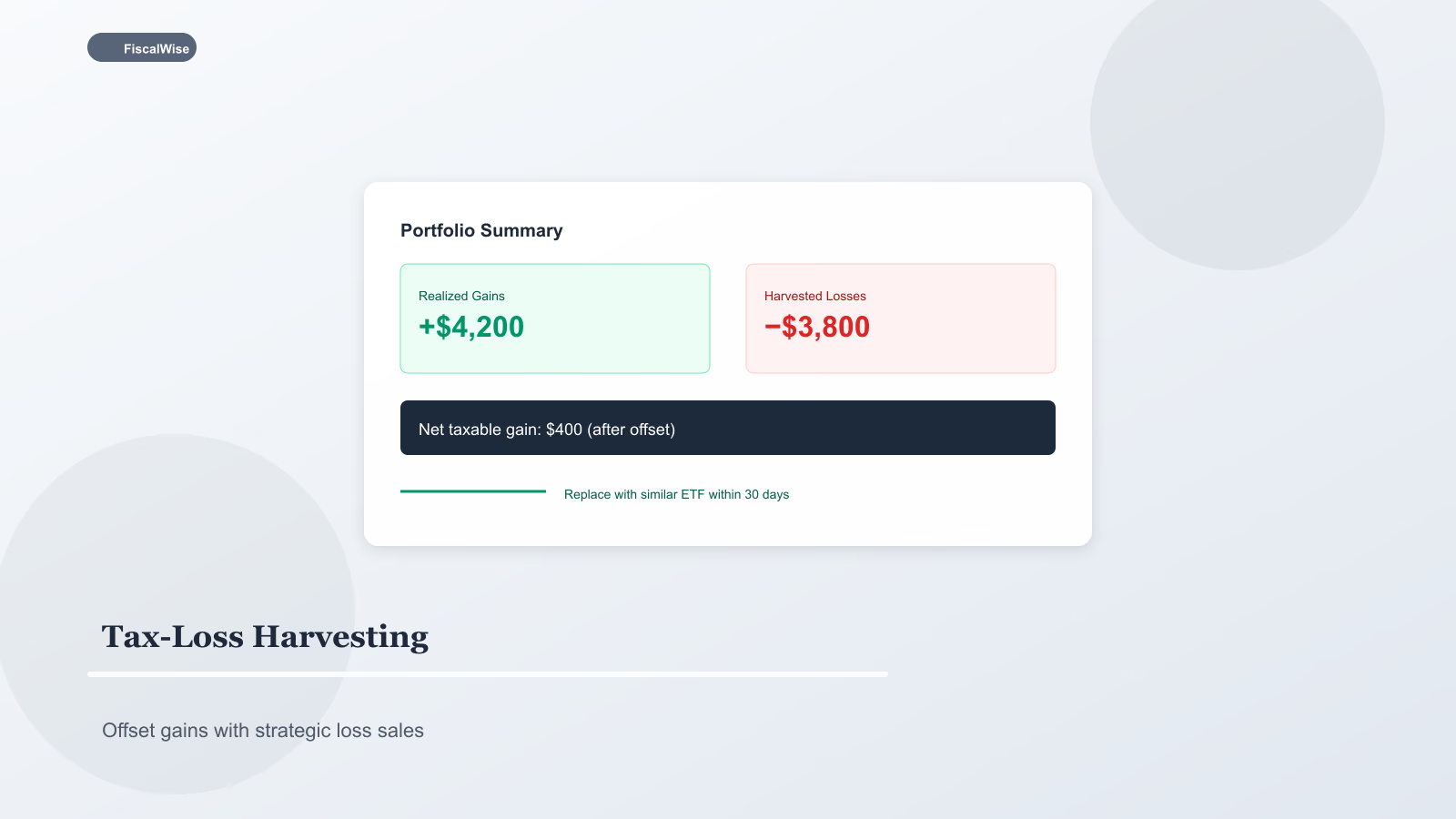

What Tax-Loss Harvesting Is

Tax-loss harvesting sells investments at a loss to offset capital gains and up to $3,000 of ordinary income per year (married filing jointly; limits vary — verify annually). Losses above limits carry forward indefinitely.

You are not "losing money on purpose" — you swap into a similar (not substantially identical) investment, maintain market exposure, and bank the tax deduction. Done well, harvesting turns volatility into a silver lining.

When It Makes Sense

Taxable brokerage accounts only — 401(k) and IRA trades do not create capital gains tax events you can harvest against.

You have realized gains this year — From stock sales, crypto (where applicable), fund distributions.

Positions are underwater — Cost basis above current value.

You can avoid wash sales — See below.

Use our investment return calculator to separate paper losses from realized performance before selling.

The Wash-Sale Rule

IRS disallows the loss if you buy a "substantially identical" security within 30 days before or after the sale — 61-day window total. That includes IRA purchases of the same stock or fund.

Safe approach: sell Vanguard Total Stock Market ETF, buy S&P 500 ETF or total market fund from different provider that tracks slightly different index — not identical share class of same fund.

Also watch spouses' accounts — wash sale applies across household purchases in many interpretations.

Offset Rules

- Short-term losses offset short-term gains first

- Long-term losses offset long-term gains

- Net losses offset other net gains

- Remaining losses: $3,000 ordinary income offset, rest carries forward

Bracket impact of ordinary offset depends on marginal rate — model with tax bracket calculator.

Robo-Advisors vs. DIY

Robo platforms automate harvesting daily in small amounts. DIY investors often harvest in November–December when year-to-date gains are visible. Both work; automation captures more micro-losses; DIY avoids robo fees.

Funds vs. Individual Stocks

Harvesting individual stocks is easier to swap without wash issues. Index ETFs need careful substitute pairs. Mutual funds may distribute taxable gains even when NAV fell — another reason ETFs dominate taxable accounts.

Do Not Let Tax Tail Wag Dog

Harvesting to offset $500 of gains while paying $15 trade commissions and spreading basis tracking headaches is false economy. Target meaningful lots; keep records.

Never sell solely for tax if you abandon desired allocation — rebuy substitute same day.

Interaction With Retirement Planning

Loss harvesting does not replace maxing IRA/401(k). Tax-advantaged space still priority. Harvesting optimizes taxable overflow after emergency fund and retirement contributions.

Year-End Playbook

- List taxable lots with cost basis and holding period

- Estimate realized gains YTD from broker 1099 preview

- Identify underwater positions with substitutes ready

- Execute sales before late December settlement cutoff

- Document trades for CPA

Tax-loss harvesting is a taxable-account technique for disciplined investors. Markets dip — harvest thoughtfully, respect wash rules, and keep long-term allocation intact.

Topics covered

- tax-loss harvesting

- capital gains

- wash sale

- tax planning

Frequently Asked Questions

What is the wash-sale rule?

IRS disallows a tax loss if you buy a substantially identical security within 30 days before or after the sale. The rule applies across your accounts and may include IRA purchases of the same security.

Can I harvest losses in my 401(k)?

No. Tax-loss harvesting applies to taxable brokerage accounts. Trades inside 401(k) and IRA do not create capital gains tax events to offset.

How much capital loss can offset ordinary income?

Net capital losses can offset up to $3,000 of ordinary income per year for married filing jointly. Excess losses carry forward indefinitely to future years.