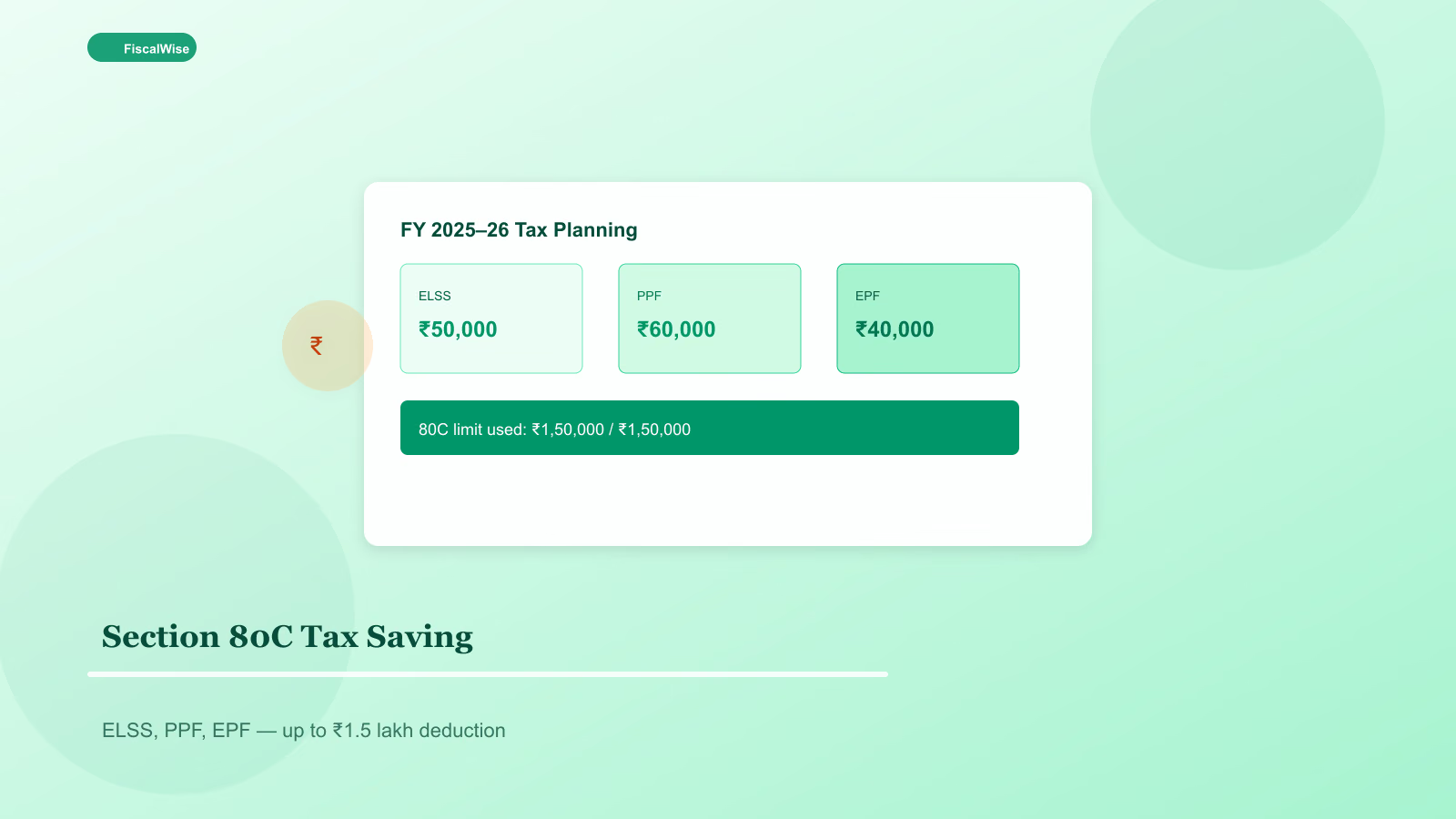

Section 80C Tax Saving in India: ELSS, PPF, EPF, and the New Tax Regime

How India's ₹1.5 lakh Section 80C deduction works, which instruments qualify, and when the old regime beats the new regime for salaried taxpayers.

Why Section 80C Still Matters for Many Salaried Indians

India's Income Tax Act lets you reduce taxable income by up to ₹1.5 lakh per financial year through qualifying investments and expenses under Section 80C. For someone in the 30% bracket (plus cess), that is meaningful tax saved — but only if you are on the old tax regime and actually use the full basket.

Since FY 2023–24, the default for many salaried employees is the new tax regime with lower slab rates but far fewer deductions. Section 80C does not apply there. The first decision each April is not which ELSS fund to pick — it is whether old or new regime saves more for your income and deduction profile.

Use our budget calculator to map monthly take-home after TDS, then model how ₹12,500/month in 80C investments fits your cash flow.

What Qualifies Under Section 80C

Common eligible items include:

| Instrument | Lock-in | Notes |

|---|---|---|

| ELSS mutual funds | 3 years | Equity-linked; shortest lock-in among 80C options |

| PPF | 15 years (extendable) | Government-backed; partial withdrawal after year 7 |

| EPF (employee share) | Until retirement | Automatic for most salaried workers |

| Life insurance premium | Policy term | Premium for self/spouse/children |

| Home loan principal | — | Principal portion of EMI, not interest |

| SSY, NSC, tax-saver FD | Varies | Popular for conservative savers |

| Tuition fees | — | Up to 2 children; full-time education |

The ₹1.5 lakh cap is combined across all 80C avenues — not per instrument.

ELSS vs PPF vs EPF: How to Think About the Mix

EPF often fills a large chunk automatically via employer and employee contributions. Check your Form 12BB and annual PF statement before chasing new products.

PPF suits long-term, risk-averse savers who want sovereign-backed returns. Interest rates are announced quarterly by the government.

ELSS is the equity route — market-linked returns with only a three-year lock-in. Pair with SIP discipline using our savings goal calculator to spread ₹1.5 lakh across 12 months instead of a March scramble.

Do not buy insurance you do not need solely for 80C. A high-commission traditional policy rarely beats ELSS + term insurance bought separately.

Section 80D, HRA, and Beyond

80C is the headline, but complete tax planning includes:

- Section 80D — health insurance premiums (self, parents, senior parents at higher limits)

- HRA exemption — if you rent and receive House Rent Allowance; keep rent receipts and landlord PAN when required

- Section 80CCD(1B) — extra ₹50,000 for NPS beyond 80C

- Standard deduction — ₹75,000 for salaried under new regime (FY 2025–26); verify current year limits

Old Regime vs New Regime: A Practical Framework

| Factor | Favour old regime | Favour new regime |

|---|---|---|

| 80C + 80D fully used | Yes | No |

| Home loan interest (24b) large | Yes | Less benefit |

| HRA exemption significant | Yes | N/A in new |

| Minimal deductions | No | Yes |

| Income under ~₹12–15 lakh with few deductions | Unlikely | Often yes |

Employers let you switch regimes at the start of the financial year. Run both scenarios with our Asia-Pacific income tax calculator before locking in.

Common Mistakes

Last-minute March lump sums — SIP through the year reduces timing risk and cash crunch.

Ignoring EPF double-counting — Do not claim the same contribution twice across Form 16 and separate proofs.

Staying on old regime without using deductions — Lower slabs in new regime may win if you leave 80C empty.

Confusing 80C with 80CCC/80CCD — NPS has separate limits; plan holistically.

Tie-In to Broader Money Habits

Tax-saving investments should align with goals — retirement, child's education, home down payment — not just March receipts. Build your emergency fund in a liquid account first; lock-in products come after the cushion exists.

Section 80C is a tool, not a strategy. Pick the right regime, automate qualifying investments, and keep proofs organised for ITR filing — that is how Indian households keep more of what they earn.

Topics covered

- Section 80C

- India tax

- ELSS

- PPF

- tax saving India

Frequently Asked Questions

What is the Section 80C deduction limit in India?

You can claim up to ₹1.5 lakh per financial year across qualifying investments and expenses under Section 80C, but only if you opt for the old tax regime.

Does Section 80C apply under the new tax regime?

No. The new tax regime offers lower slab rates but does not allow most deductions including Section 80C. Compare both regimes with your actual investments before choosing.

What is the best Section 80C investment?

There is no single best option — EPF may fill automatically, PPF suits conservative long-term savers, and ELSS offers equity exposure with a three-year lock-in. Match instruments to your goals and risk tolerance.

Can I claim both ELSS and PPF under 80C?

Yes, but the combined deduction cannot exceed ₹1.5 lakh. EPF, life insurance premiums, and home loan principal also count toward the same cap.