UK Stocks and Shares ISA Basics: Tax-Free Investing Explained

How the UK Stocks and Shares ISA works, annual allowance rules, and a simple fund-based approach for new investors.

What a Stocks and Shares ISA Is

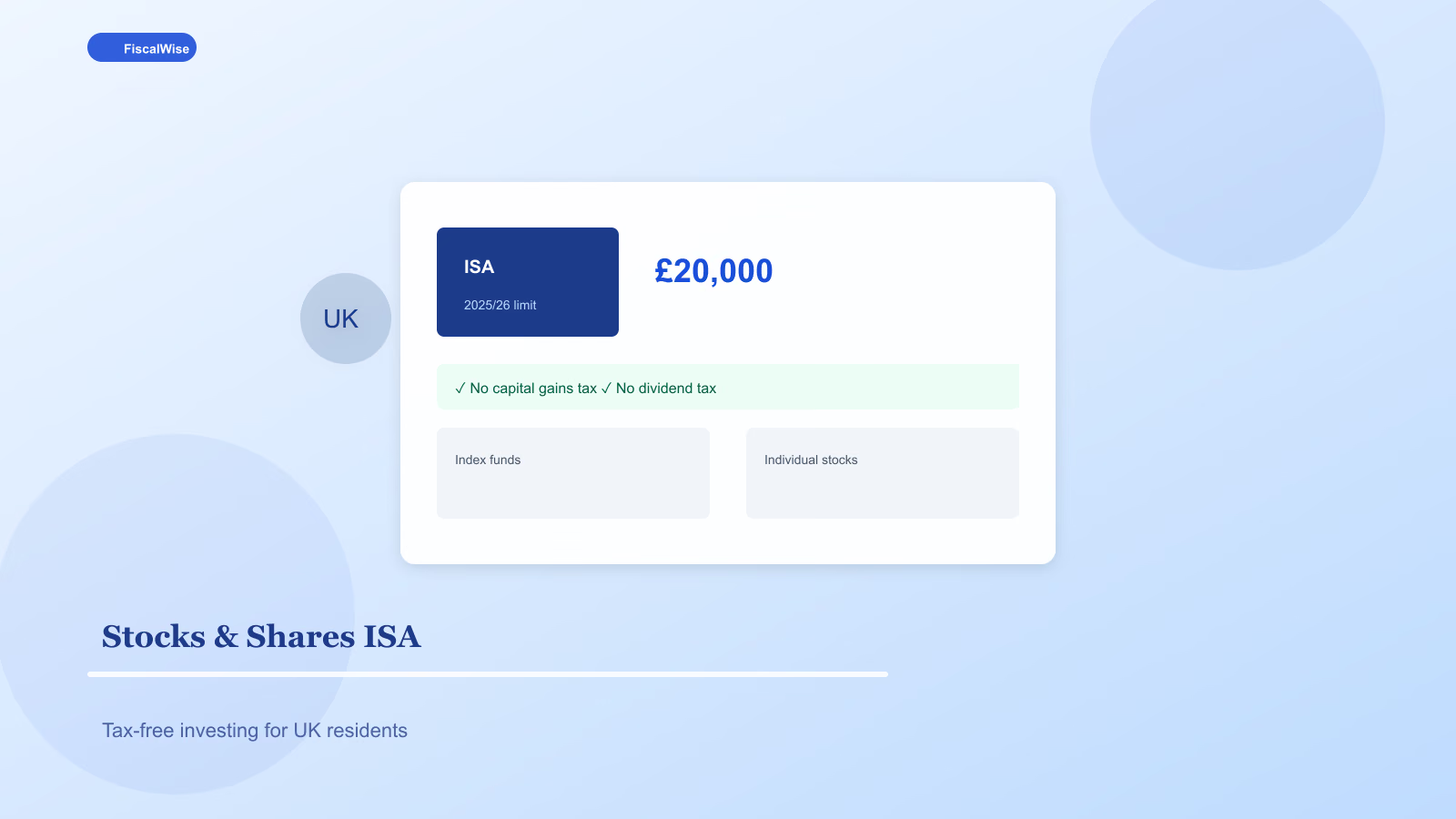

A Stocks and Shares ISA is a UK tax wrapper — not an investment itself. Hold funds, ETFs, or individual shares inside it and pay no capital gains tax on gains, no further tax on dividends inside the wrapper, and no reporting hassle for ISA-internal trades. You still risk losing money if investments fall; the ISA only removes tax friction.

The companion Cash ISA covers savings interest. You get one overall ISA allowance per tax year (6 April – 5 April) to split between cash and stocks as you choose.

Annual Allowance and Rules

For 2025/26 and 2026/27 the ISA allowance is £20,000. You can:

- Put all £20,000 in Stocks and Shares

- Split between Cash and Stocks ISAs

- Open one Stocks and Shares ISA per tax year across providers — but transfer old ISAs carefully; do not cash out and re-deposit (that burns allowance)

Junior ISAs are separate — £9,000 allowance for under-18s.

Why Use ISA Before General Investment Account

Outside an ISA, dividends above the dividend allowance and capital gains above the CGT allowance create tax paperwork. Inside ISA, compounding stays untouched by HMRC for decades. For long-term wealth building, filling ISA first is standard UK advice for most earners.

Project growth with our compound interest calculator — tax-free compounding vs. taxable drag widens over 20 years.

Choosing Investments Inside the ISA

Beginner-friendly approach:

| Holding | Role |

|---|---|

| Global equity index fund | Core growth |

| UK bond index or gilt fund | Stability ballast |

| Or single target-date / multi-asset fund | Hands-off |

Platforms like Vanguard, Hargreaves Lansdown, Trading 212, Freetrade, and ii differ on fees, fund range, and UI. Compare platform fee + fund OCF (ongoing charge figure). A 0.15% platform fee plus 0.20% fund beats 0.45% everywhere.

ISA vs. Pension (SIPP / Workplace)

| Account | Access | Tax treatment |

|---|---|---|

| ISA | Anytime | No upfront relief; tax-free growth |

| Pension | Usually 55+ rising to 57 | Upfront tax relief; taxed on withdrawal |

ISA is flexibility — house deposit in 8 years, semi-retirement bridge. Pension is maximum tax relief for locked long-term savings. Most UK workers need both.

Bed and ISA / Transfers

Moving investments from a general account to ISA uses allowance — sell, contribute cash, rebuy inside ISA. "Bed and ISA" services at brokers automate with one tax event. ISA-to-ISA transfers preserve history without using new allowance — use official transfer forms, never withdraw.

Inflation and Real Returns

Cash ISAs rarely beat inflation long-term. Stocks and Shares ISA equity allocation targets real growth above CPI. Check purchasing power with an inflation calculator when setting goals.

Common Mistakes

Trading too much — Platform fees and spread eat returns; indexes beat churn.

Ignoring allowance deadline — Allowance does not roll over. Use it or lose it each 5 April.

US dividend withholding — Some US funds still have 15% US withholding inside ISA; choose Ireland-domiciled ETFs if optimising (advanced).

Confusing ISA with gambling — Meme stocks in ISA still lose money; tax wrapper is not edge.

Getting Started This Tax Year

- Open Stocks and Shares ISA with low-cost platform

- Set monthly direct debit — DCA £200–£500 if full £20k is unrealistic

- Buy one global index until you learn rebalancing

- Increase contributions before April if allowance remains

The Stocks and Shares ISA is the UK's simplest tax-efficient investing lane. Boring funds, steady contributions, full allowance when possible — that is the playbook.

Topics covered

- Stocks and Shares ISA

- UK investing

- ISA allowance

- tax-free