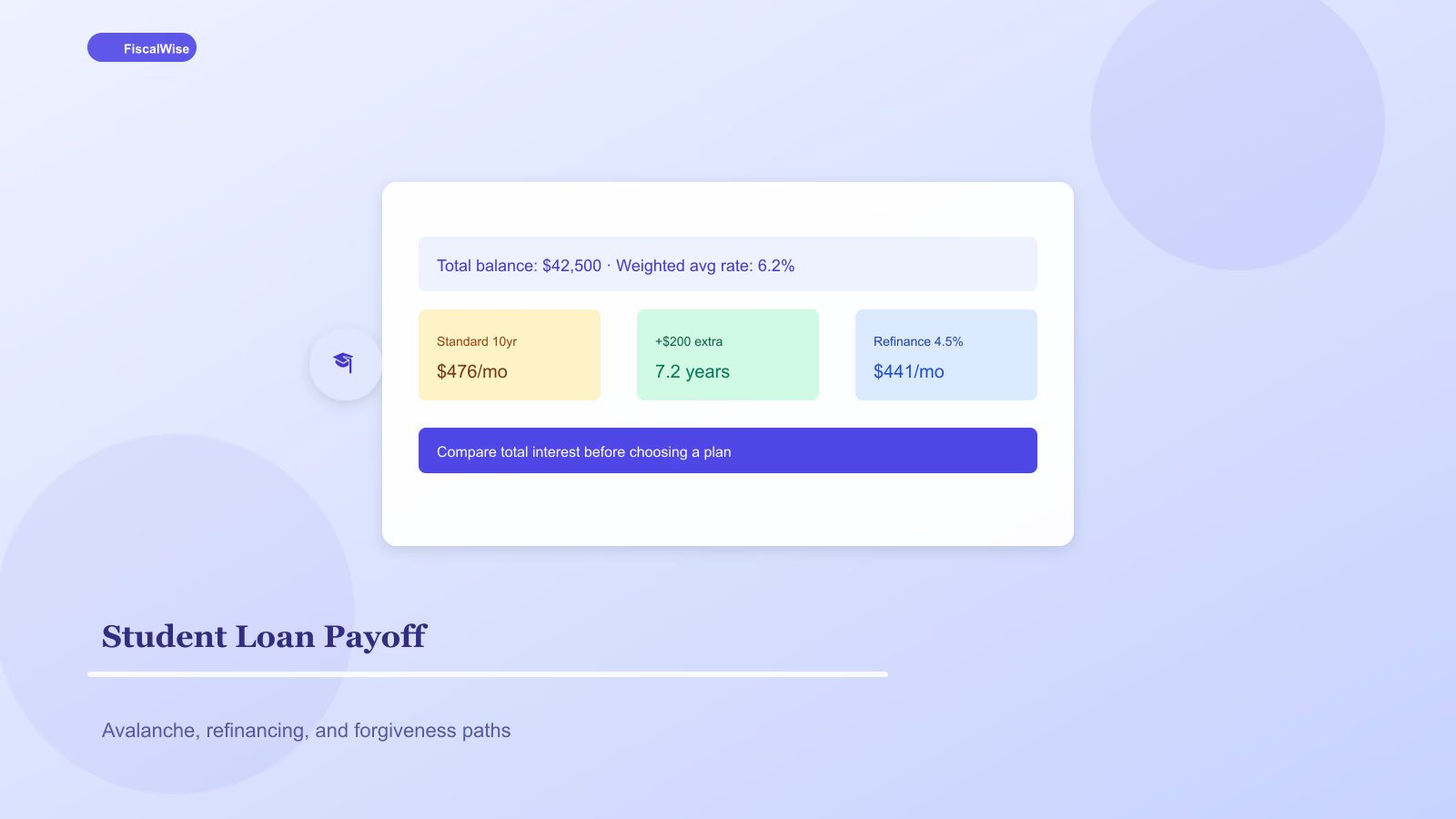

Student Loan Payoff Strategies: Avalanche, Refinance, and Forgiveness Paths

Compare federal repayment plans, private refinance tradeoffs, and PSLF — without treating all student debt the same.

Federal vs. Private: Different Playbooks

Federal student loans carry income-driven repayment (IDR), deferment, forgiveness programs, and fixed protections. Private loans are bank contracts — fewer safety nets, sometimes lower rates for high-credit borrowers.

Strategy starts with listing every loan: servicer, balance, rate, type (federal/private), forgiveness eligibility.

Payoff Method: Avalanche Usually Wins

Extra payments above minimums should target highest APR loan while staying current everywhere else — classic avalanche. Our debt payoff calculator models multiple loans; federal loans can be targeted individually within the federal portfolio.

Snowball smallest balance if psychology demands — math cost usually smaller than credit cards.

Income-Driven Repayment (IDR)

Plans cap payment at percentage of discretionary income — SAVE, PAYE, IBR, ICR. Extend timeline, may forgive remainder after 20–25 years (taxable forgiveness event possible — plan for tax bomb on forgiven balance).

Good when cash flow is tight or PSLF path exists. Bad when high income makes standard plan cheaper and faster.

Public Service Loan Forgiveness (PSLF)

120 qualifying payments on Direct Loans while working full-time for qualifying employer — government, 501(c)(3), some healthcare. Certify employment annually. Wrong plan or wrong loan type wastes years.

Do not refinance federal loans private if PSLF is on the table.

Refinancing Private (and Sometimes Federal)

Refinance replaces loans with new private loan at new rate/term. Wins when:

- Stable high income

- Credit score 700+

- No need for IDR or forgiveness

- Rate drop 1%+ worth lost protections

Compare monthly payment and total interest with loan payment calculator before and after.

Employer Repayment Benefits

Some employers pay $100–$500 monthly toward loans — free acceleration. Know tax treatment.

Biweekly Payments and Round-Ups

Biweekly half-payments yield extra full payment yearly on installment math — modest boost. Round-up apps micro-pay — fine if they do not replace larger intentional extra payments.

Side Income Allocation

Freelance income dedicated purely to highest-rate loan creates visible progress. Convert hourly gigs with salary to hourly converter to see if side effort beats overtime at day job after taxes.

Do Not Neglect Retirement for 4% Loans

Mathematically, 7% expected retirement return beats 4% loan interest — but match beats both. Minimum order:

- Employer 401(k) match

- Emergency fund starter

- High-rate private loans (>6–7%)

- Max tax-advantaged retirement

- Extra federal low-rate loans vs. invest — preference call

Default and Rehabilitation — If You Are Behind

Federal default has rehabilitation and consolidation paths — credit and wage garnishment stakes too high to ignore. Contact servicer immediately; scammers target distressed borrowers.

Consolidation Caveats

Federal consolidation simplifies to one payment; weighted average rate — does not lower rate. May reset PSLF payment count if done wrong. Direct Consolidation needed for some forgiveness paths — research before clicking.

Closing Thought

Student loans are marathon debt. Pick a strategy aligned with forgiveness, job stability, and rates — then automate extra payments and revisit yearly when income jumps. The goal is paid off or forgiven with eyes open, not surprise tax bills or lost years of PSLF credit.

Topics covered

- student loans

- PSLF

- refinance

- loan repayment

Frequently Asked Questions

Should I refinance federal student loans to private?

Only if you have stable income, strong credit, no need for income-driven repayment or forgiveness, and a materially lower rate. Refinancing federal loans permanently forfeits PSLF, IDR, and federal deferment protections.

What is Public Service Loan Forgiveness?

PSLF forgives remaining federal Direct Loan balance after 120 qualifying payments while working full-time for a qualifying government or nonprofit employer. Certify employment annually and use an eligible repayment plan.

Is it better to pay extra on student loans or invest?

Get employer 401(k) match first. Then compare loan APR to expected investment return. Loans above 6–7% often deserve aggressive payoff; low-rate federal loans may yield to retirement investing after emergency fund is solid.