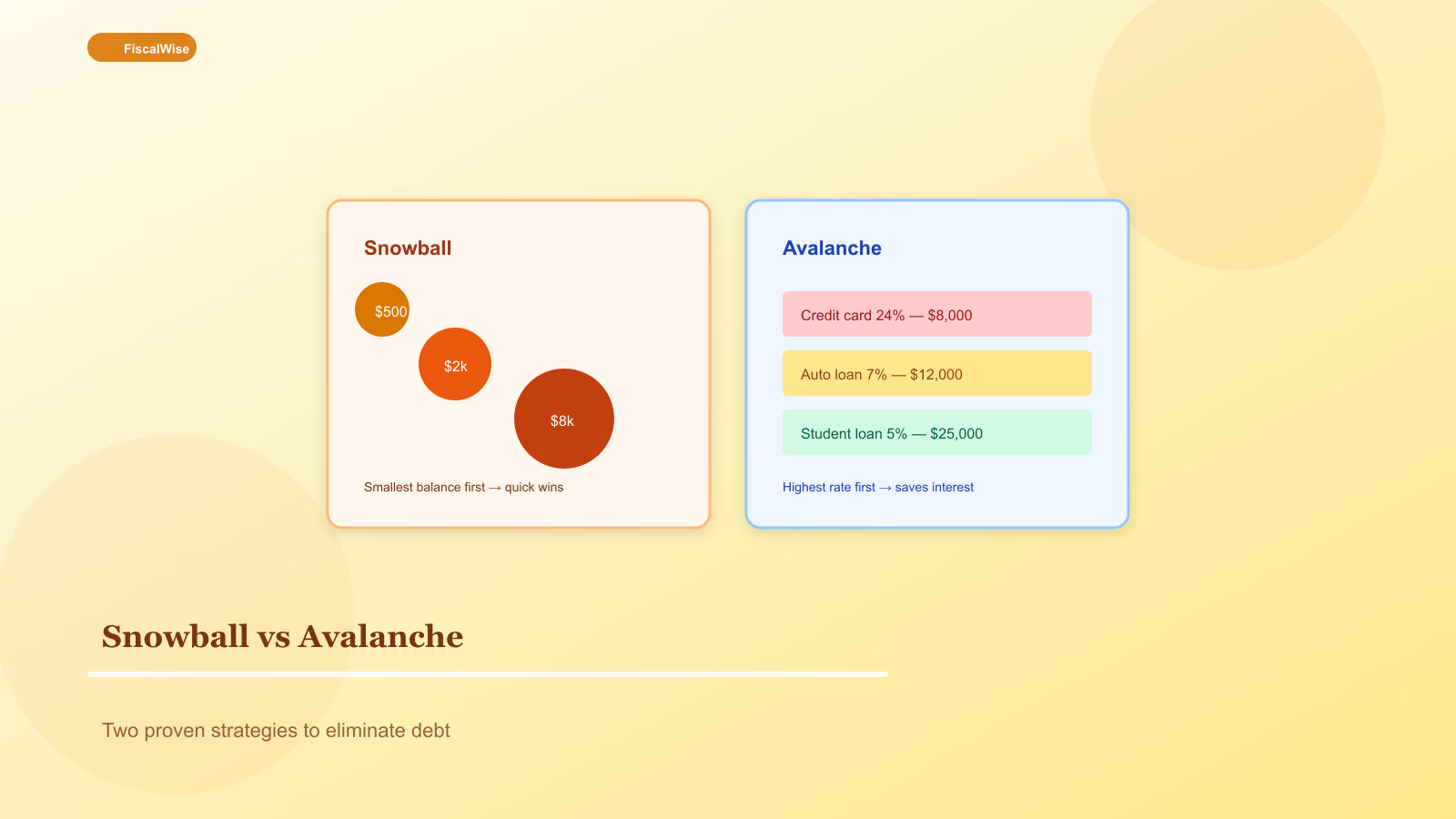

Debt Snowball vs. Avalanche: Which Payoff Method Saves More?

Compare psychological wins and mathematical savings when attacking multiple debts — and how to pick the method you will finish.

Two Valid Ways to Kill Debt

You have multiple debts and one extra payment each month. Snowball pays smallest balance first regardless of APR. Avalanche pays highest interest rate first regardless of balance. Both pay minimums on everything else.

Mathematically, avalanche almost always saves more interest and finishes sooner — sometimes by months, sometimes by years on large card stacks.

Behaviorally, snowball closes accounts faster, creating dopamine that keeps people paying extra when life gets loud.

The best method is the one you complete.

Side-by-Side Example

| Debt | Balance | APR | Min payment |

|---|---|---|---|

| --- | ---: | ---: | ---: |

| Card A | $800 | 24% | $25 |

| Card B | $4,200 | 18% | $85 |

| Card C | $1,500 | 12% | $40 |

Extra payment: $200/month beyond minimums.

Snowball order: A → C → B. Card A gone in ~3 months — celebration, one less bill.

Avalanche order: A → B → C (A and B tie on APR priority — if A higher, same first). B attacked before C despite smaller C balance.

Run your actual stack through our debt payoff calculator — enter every balance, rate, and minimum. Toggle methods; compare total interest and payoff dates.

When Snowball Wins Despite Math

- You need early wins to trust the process

- Smallest debts are store cards with annoying minimums

- Couples need shared visible progress on kitchen whiteboard

- History of quitting debt plans when progress feels invisible

Interest difference might be $400 over two years — meaningful but not if snowball prevents $2,000 in new charges from giving up.

When Avalanche Is Clear Choice

- Large rate spreads — 29% card vs. 7% student loan

- High discipline, past success with long goals

- Balances similar sizes — psychology equal, math dominates

- You are motivated by spreadsheets, not closed-account parties

Hybrid and Modified Approaches

Debt landslide — Highest rate first, but if two rates within 1%, pick smaller balance.

One quick win then avalanche — Pay $800 card first regardless, then strict avalanche.

Emotional anchor — Never close oldest card if it helps credit age; pay to zero and stop using.

Credit Card Interest Context

Minimum payments mostly feed interest. See true cost with credit card interest calculator — $3,000 at 24% with $90 minimum can take 4+ years and thousands in interest.

Student and Auto Loans in the Mix

Avalanche usually prioritizes cards over 5% student loans. Auto loans are secured — falling behind risks repossession; keep minimums current even if avalanche targets cards first.

For single large installment debt, use loan payment calculator to see if refinancing beats accelerated payoff.

Staying Out of Debt After

- Build one-month buffer, then full emergency fund

- Remove saved card numbers from browsers

- Use debit or one paid-in-full card

- Budget with budget calculator so minimums are not "extra"

The Verdict

Choose avalanche if you will stick without quick wins. Choose snowball if past attempts died with the biggest balance still staring at you. Run the numbers, pick, automate extra payments, and do not restart the debate every month.

Debt freedom date matters more than debating methods on Reddit. Snowball and avalanche both get you there — start this week.

Topics covered

- debt snowball

- debt avalanche

- debt payoff

- credit cards

Frequently Asked Questions

Which saves more money — snowball or avalanche?

Avalanche almost always pays less total interest and finishes sooner because it targets highest APR first. The gap can be hundreds or thousands depending on balances and rate spreads.

Why do some people choose debt snowball anyway?

Closing small balances quickly creates psychological wins that keep people paying extra. If avalanche history includes quitting when the biggest balance barely moves, snowball may succeed where math alone failed.

Should I pay off student loans or credit cards first?

Usually credit cards first — higher APR and no asset backing. Keep minimums current on all debts, then direct extra payments to the highest-rate loan unless pursuing specific federal forgiveness programs.

Can I switch from snowball to avalanche mid-plan?

Yes. Re-run your balances through a payoff calculator and pick the method you will stick with. Consistency matters more than the label.