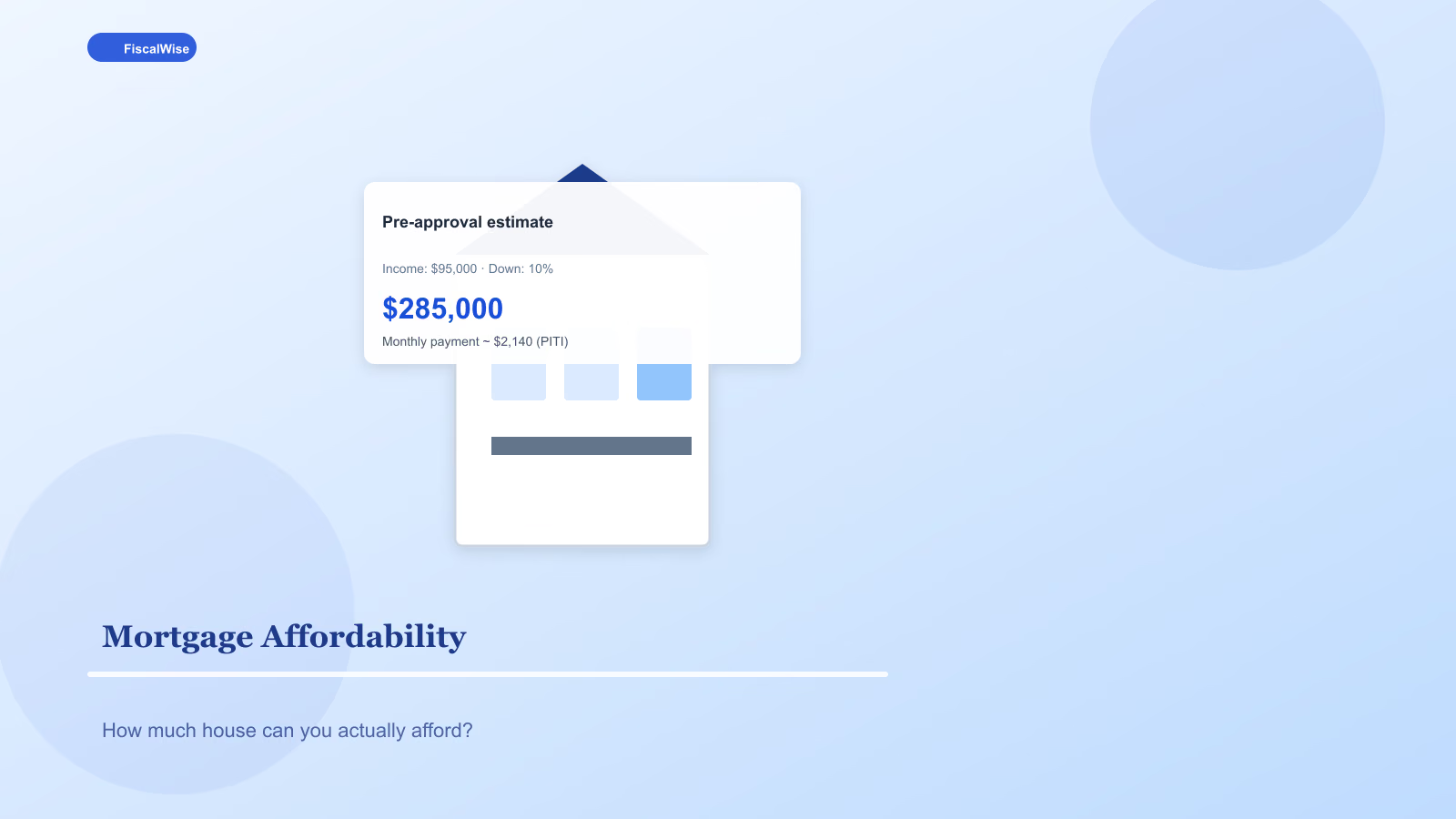

Mortgage Affordability for First-Time Buyers: How Much House Can You Afford?

DTI ratios, down payment tradeoffs, and hidden costs beyond P&I — a reality check before open houses.

Affordability Is Not What the Bank Maxes You At

Lenders approve based on debt-to-income ratio (DTI) — often up to 43–50% total debt payments vs. gross income. That includes car loans, student loans, credit cards, and the new mortgage with taxes and insurance.

You can be approved for more house than you can live in comfortably. Groceries, childcare, retirement, and a single HVAC repair do not appear in DTI. Buy below approval ceiling.

The 28/36 Rule as Sanity Check

Classic guidelines:

- Housing costs ≤ 28% of gross monthly income (P&I + taxes + insurance + HOA)

- All debt ≤ 36% of gross including housing

On $8,000 gross monthly income, 28% is $2,240 housing, 36% is $2,880 total debt. If student and car loans are $600, housing budget near $2,280 under strict 36% cap.

Run numbers in our mortgage calculator — enter price, down payment, rate, term for P&I, then add tax and insurance estimates locally.

Down Payment: 3%, 10%, or 20%?

| Down % | Pros | Cons |

|---|---|---|

| ---: | --- | --- |

| 3–5 (FHA/conventional low) | Sooner purchase, keep cash reserves | PMI, higher payment |

| 10 | Balance | PMI may remain |

| 20 | No PMI, lower payment | Ties cash in equity |

Emptying emergency fund for 20% down is risky. Better 10% down plus six-month reserve than 20% down with $0 buffer.

PITI and the Hidden Costs

Principal & Interest — What calculators show.

Property taxes — 0.5–2.5%+ of value yearly depending on locale.

Insurance — Homeowners + flood if required.

HOA — Can be $200–$800+ monthly in condos.

Maintenance — Budget 1–2% of home value yearly — roof, appliances, pest.

Utilities — Often higher than apartment — heat, lawn, trash.

Pair P&I with budget calculator full household picture before falling for listing photos.

Rate Shopping and Points

0.25% rate difference on $350k loan is tens of thousands over 30 years. Get Loan Estimates from multiple lenders same week — hard pulls within 14–45 days often count as one inquiry for scoring.

Adjustable-rate mortgages (ARMs) suit short ownership horizons only — know reset risk.

First-Time Buyer Programs

State and local down payment assistance, FHA 3.5%, VA 0% for eligible veterans, USDA rural zero down. Income caps and education courses apply — research before assuming.

Pre-Approval vs. Pre-Qualification

Pre-approval with documented income and credit is stronger for offers. Shop lenders before realtors push in-house partner — comparison saves money.

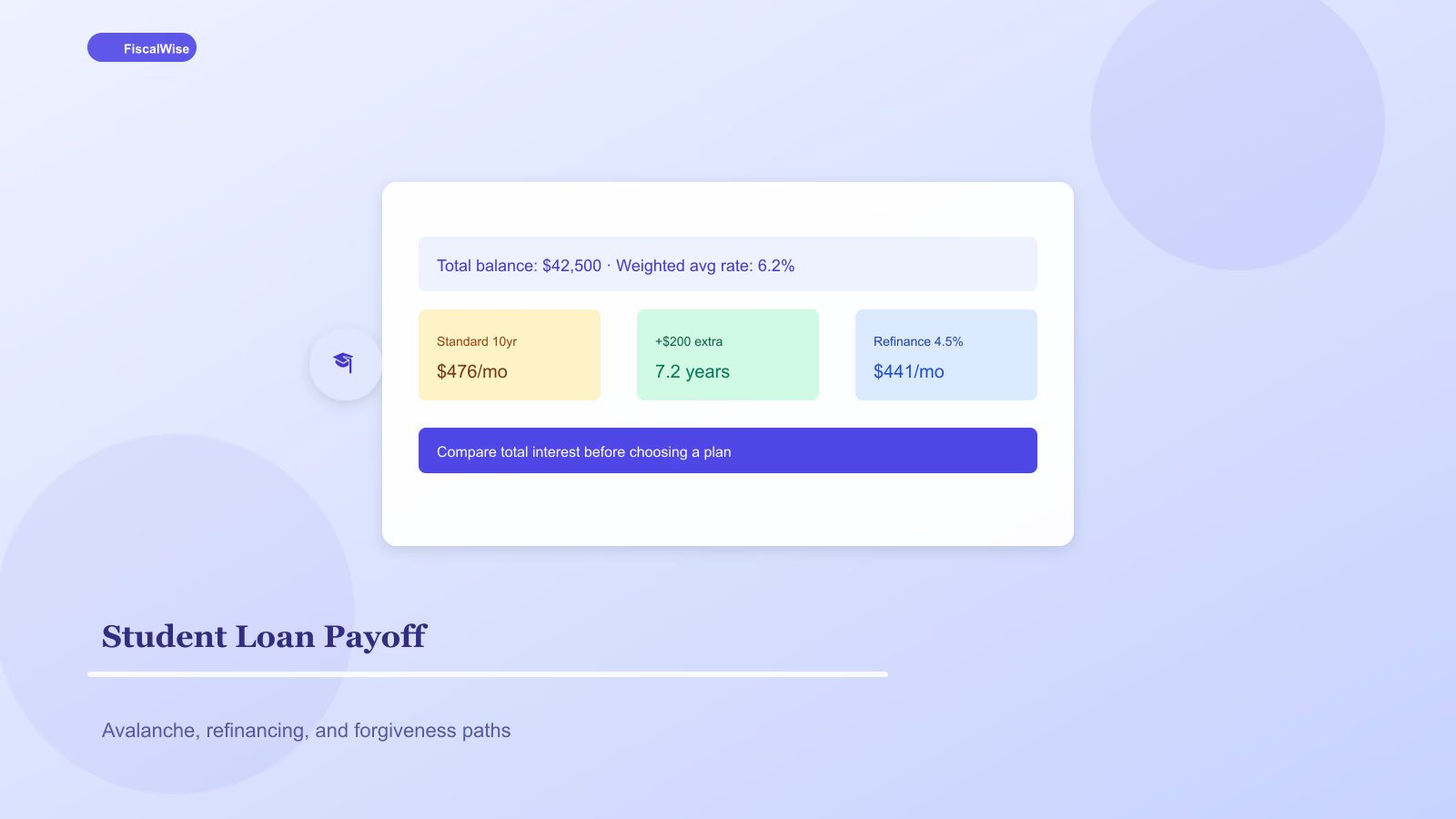

Student Loans and DTI

Income-driven repayment plans use payment on credit report — sometimes lower than standard amortization, helping DTI. Payoff strategy interacts; see student loan guide.

Use loan payment calculator for auto and personal debts eating DTI room.

When to Wait

- Emergency fund under three months

- Credit score under 620 without FHA path

- Job instability within 12 months

- Planning move within 3 years — transaction costs need 5+ year horizon typically

A Worked Example

$95k household income ($7,917/mo gross). Target 28% housing = $2,217.

At 6.5% rate, 30-year, $40k down:

- $320k purchase → ~$1,770 P&I + $400 tax/insurance ≈ $2,170 — fits

- $380k purchase → ~$2,100 P&I + $480 tax/insurance ≈ $2,580 — strains other goals

Adjust price until payment leaves room for life.

Mortgage affordability is monthly cash flow plus resilience, not lender maximum. Calculate PITI honestly, keep reserves, and leave margin for the water heater that dies the week you move in.

Topics covered

- mortgage affordability

- first-time buyer

- DTI

- home buying

Frequently Asked Questions

What debt-to-income ratio do lenders use for mortgages?

Many lenders cap total debt payments — housing plus other debts — around 43–50% of gross monthly income. Housing alone is often evaluated near 28% of gross, though programs vary.

Do I need 20% down to buy a first home?

No. Conventional loans allow as little as 3% down for qualified first-time buyers; FHA allows 3.5%. Twenty percent avoids private mortgage insurance but should not drain your entire emergency fund.

What costs beyond the mortgage payment should I budget?

Property taxes, homeowners insurance, HOA fees, maintenance (1–2% of home value yearly), higher utilities, and closing costs. P&I alone understates true ownership cost.

How much house can I afford on $80,000 income?

Using the 28% rule on gross monthly income near $6,667, target housing costs around $1,867 per month including taxes and insurance. Exact purchase price depends on down payment, rate, and local tax rates — run scenarios in a mortgage calculator.