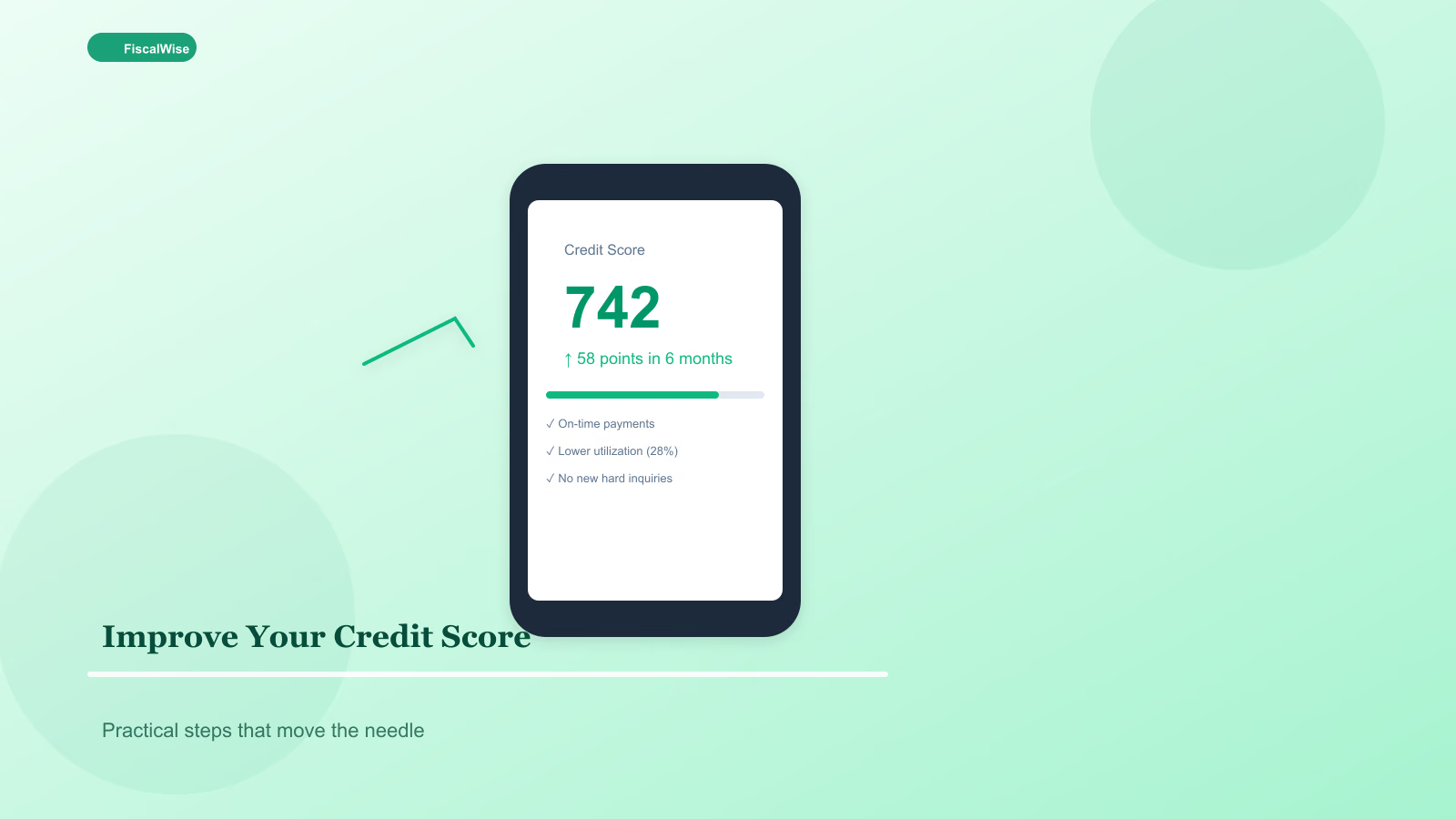

How to Improve Your Credit Score Fast: Practical Steps That Work

Legitimate tactics to raise FICO and VantageScore — utilization, payment history, and errors to dispute — without credit repair scams.

What Actually Moves Your Score

FICO and VantageScore weight:

| Factor | Approx. weight |

|---|---|

| --- | ---: |

| Payment history | 35% |

| Amounts owed (utilization) | 30% |

| Length of credit history | 15% |

| New credit | 10% |

| Credit mix | 10% |

"Fast" improvements usually mean fixing utilization and errors — not overnight 100-point magic. Late payments age off over seven years; there is no legitimate delete for accurate lates.

Quick Win 1: Lower Utilization Below 30%, Then 10%

Utilization is balances ÷ credit limits on revolving accounts. $3,000 balance on $10,000 limits = 30%.

Pay down cards before statement closing date — balances reported to bureaus often reflect statement balance, not what you pay after.

Micro-tactics:

- Pay twice monthly

- Request credit limit increase without new hard pull (issuer dependent)

- Spread charges across two cards vs. maxing one

Model card interest cost while paying down with credit card interest calculator.

Quick Win 2: Autopay Minimums, Manual Extra

One missed payment can drop scores 50–100+ points. Autopay at least minimum on every account; manually add extra to highest APR.

Quick Win 3: Dispute Accurate-Inaccurate Items

Pull free reports from AnnualCreditReport.com. Dispute wrong balances, duplicate accounts, not-your accounts. Bureaus have 30 days to investigate.

Avoid credit repair mills charging $99/month to dispute everything — re-disputing accurate debt fails.

Quick Win 4: Authorized User Status

Trusted family member adds you as authorized user on old, low-utilization card. Their history may appear on your report — risk is their mistakes hurt you too.

What Not to Do

Close old cards — Hurts utilization and average age unless fee is brutal and limit is tiny.

Open six store cards for discounts — Hard inquiries and young accounts ding score short-term.

Consolidate to one maxed card — Utilization worse than spread balances.

Debt Payoff and Score Interaction

Paying off installment loans can briefly dip score — mix changes — but long-term win is less debt. Use debt payoff calculator for plan; score follows in months as utilization falls.

Building Credit From Thin File

- Secured card with $200–$500 deposit

- Credit-builder loan from credit union

- Report rent via services landlords support (where available)

Patience required — six months minimum for meaningful thickening.

Mortgage and Auto Timing

Scores affect APR dramatically. 680 vs. 740 on $300k mortgage can mean tens of thousands in interest — see mortgage calculator at different rate scenarios.

Improve score before applying if purchase is 6+ months out.

Track Net Worth Alongside Score

Score is borrowing reputation; net worth is wealth. Net worth calculator keeps focus on assets growing while score repairs.

Realistic Timeline

| Action | Typical impact window |

|---|---|

| Pay down utilization | 1–2 billing cycles |

| Dispute error removal | 30–45 days |

| Authorized user | 1–2 months |

| Good behavior compound | 6–12 months |

Improving credit is boring: pay on time, owe less, fix mistakes, wait. That beats scams promising deleted bankruptcies by Tuesday. Your future self gets cheaper loans — start with statement-date payments this month.

Topics covered

- credit score

- FICO

- credit utilization

- credit repair

Frequently Asked Questions

How fast can credit utilization changes affect my score?

Lowering reported balances often shows within one to two billing cycles because utilization is a major scoring factor. Pay before statement closing date so bureaus see lower balances.

Will paying off a loan hurt my credit score?

Closing an installment loan can briefly lower score by changing credit mix and average age, but reducing overall debt is positive long-term. Do not keep loans open just for score if you can pay them off.

Do credit repair companies work?

Legitimate disputes of inaccurate items work for free by contacting bureaus yourself. Companies charging monthly fees to dispute accurate negative items rarely deliver lasting results.

What utilization percentage is ideal?

Under 30% per card and overall is good; under 10% is excellent for maximizing score. Spread charges across cards rather than maxing one account.