Retirement Account Contribution Limits for 2026: 401(k), IRA, and HSA

Updated 2026 caps for workplace plans, IRAs, catch-up contributions, and how to prioritize accounts when you cannot max everything.

Why Limits Change Every Year

IRS adjusts retirement contribution limits for inflation and policy. Hitting the max is optional — most people cannot — but knowing caps helps you prioritize employer match, tax-advantaged space, and catch-up windows at 50+.

Figures below reflect 2026 planning numbers; confirm on IRS.gov when filing.

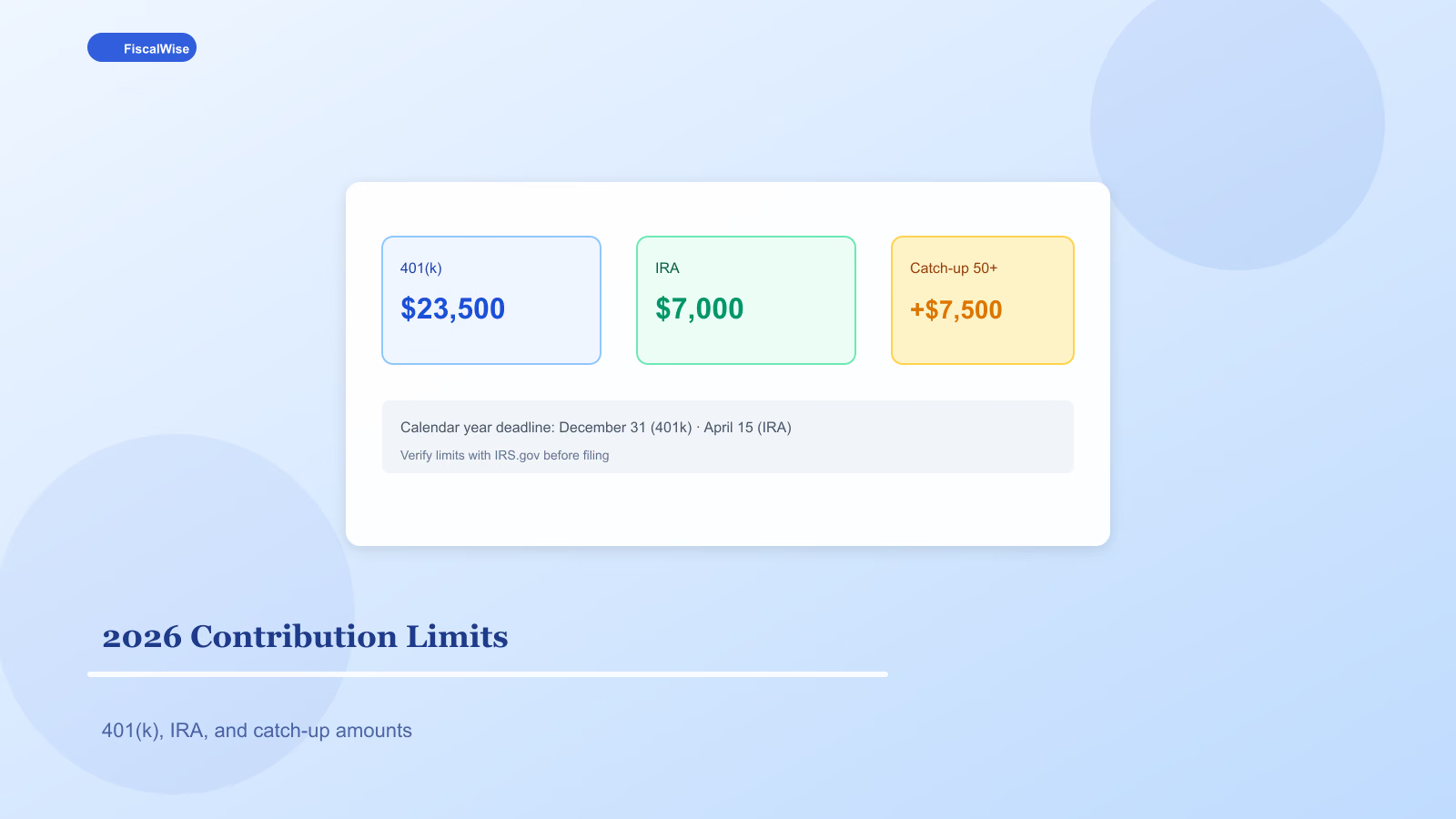

2026 Workplace Plan Limits (401k, 403b, 457)

| Limit type | Amount |

|---|---|

| --- | ---: |

| Employee elective deferral | $24,500 |

| Catch-up (age 50+) | +$8,000 |

| Total annual additions (employee + employer) | $70,000 |

High earners face additional nondiscrimination testing; HCE limits may apply in your plan.

IRA and Roth IRA

| Limit type | Amount |

|---|---|

| --- | ---: |

| Combined IRA contribution | $7,500 |

| Catch-up (age 50+) | +$1,100 |

Roth income phaseouts apply — backdoor Roth may help if income exceeds direct Roth eligibility; consult CPA for pro-rata rules.

HSA (Health Savings Account)

| Limit type | Amount |

|---|---|

| --- | ---: |

| Self-only coverage | $4,400 |

| Family coverage | $8,750 |

| Catch-up (55+) | +$1,000 |

Must have qualifying high-deductible health plan (HDHP). Triple tax advantage: deductible contribution, tax-free growth, tax-free qualified medical withdrawals.

Priority Stack When Cash Is Limited

- 401(k) to employer match — 50–100% instant return

- HSA if HDHP — if you can pay current medical from cash and invest HSA

- Roth or traditional IRA — $7,500 room, flexible investments

- 401(k) beyond match — finish to $24,500 if possible

- Taxable brokerage — after tax-advantaged lanes

Project outcomes with retirement savings calculator at current contribution vs. maxed scenario — gap motivates raises and budget trims.

FIRE and Early Retirement Implications

Aggressive savers maxing 401(k) + IRA + HSA need taxable bridge for years before 59½. Our FIRE calculator estimates independence number; contribution limits tell you how fast you fill tax-sheltered buckets each year.

Mega Backdoor Roth (Advanced)

Some 401(k) plans allow after-tax contributions beyond $24,500 elective deferral up toward $70,000 total, then in-plan Roth conversion. Not universal — check SPD or HR.

Solo 401(k) for Self-Employed

Business owners without employees may contribute as employee plus employer profit share — potentially much higher than employee limit alone. Setup required by December 31 typically.

Tax Bracket Coordination

Traditional 401(k) contributions reduce taxable income — worth more in 24% bracket than 12%. Model with tax bracket calculator before stuffing traditional vs. Roth 401(k) elections in open enrollment.

Calendar Reminders

- January — Reset payroll percentages for new limits

- April — Prior-year IRA deadline

- October–November — Open enrollment; bump 401(k) 1% if behind

- December — Last chance for 401(k) deferrals and HSA contributions for tax year

Contribution limits are the guardrails — not the goal. Match first, automate increases, and treat each raise as split between lifestyle and one more percent to retirement.

Topics covered

- 401k limits

- IRA limits

- HSA

- retirement contributions 2026

Frequently Asked Questions

What is the 401(k) contribution limit for 2026?

The employee elective deferral limit is $24,500 for 2026, with an additional $8,000 catch-up contribution for participants age 50 and older.

Can I contribute to both 401(k) and IRA?

Yes. 401(k) and IRA limits are separate. IRA deductibility and Roth eligibility may phase out based on income and workplace plan participation.

What should I fund first — 401(k) or IRA?

Contribute to your 401(k) at least through the employer match, then consider IRA for investment flexibility, then return to max 401(k) if cash flow allows.