UK Personal Allowance and Income Tax Guide for 2026/27

How the UK personal allowance, basic and higher rate bands work — and what changes when income passes £100,000.

UK Income Tax in Plain English

UK employees pay income tax on earnings above the personal allowance through PAYE — deducted before salary hits the bank. Scotland has different bands; this guide covers England, Wales, and Northern Ireland unless noted.

Three concepts matter: personal allowance (tax-free slice), marginal rate on the next pound, and effective rate across all income.

Personal Allowance and Taper

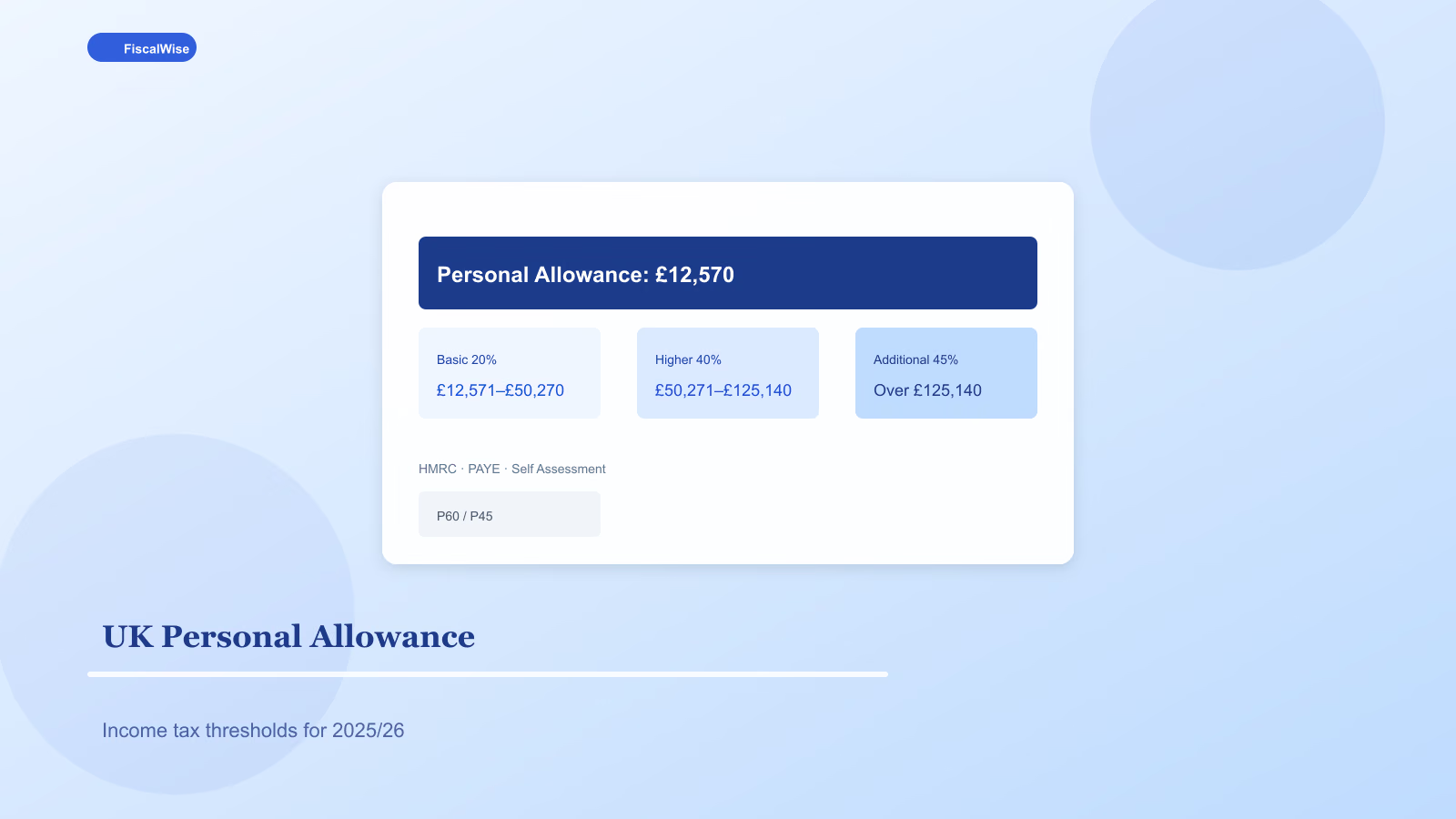

For 2026/27 planning, the standard personal allowance is £12,570. You pay 0% on income within it (savings and dividend allowances are separate).

£100,000 trap: Allowance reduces by £1 for every £2 earned above £100,000 until gone near £125,140. Effective marginal rate in that zone can exceed 60% when accounting for lost allowance — pension contributions and salary sacrifice shine here.

Main Tax Bands (England, Wales, NI)

| Band | Taxable income (approx.) | Rate |

|---|---|---|

| --- | --- | ---: |

| Personal allowance | £0 – £12,570 | 0% |

| Basic rate | £12,571 – £50,270 | 20% |

| Higher rate | £50,271 – £125,140 | 40% |

| Additional rate | over £125,140 | 45% |

Dividends and savings have separate rate schedules and allowances.

Salary Sacrifice and Pension Relief

Pension contributions via salary sacrifice reduce taxable income and National Insurance — powerful above higher-rate threshold. Contributing enough to stay under £50,270 basic-rate ceiling saves 40% vs. 20% on marginal pounds.

Compare gross packages with our salary to hourly converter and rough tax estimates for side gigs.

Self-Assessment When PAYE Is Not Enough

Self-employed, landlords, high dividend earners, and £100k+ with complex income file Self Assessment. Payments on account January and July — budget sinking funds accordingly.

ISAs and Tax Wrappers

Stocks and Shares ISA gains do not use personal allowance or CGT — see our ISA basics guide. Still fund ISA after workplace pension if employer match exists.

National Insurance (Brief)

NI is separate from income tax — employee Class 1 on earned income, rates and thresholds change in Budgets. Total marginal "tax" includes NI; use HMRC calculators for precision.

Planning Moves

Just below higher rate — Pension top-up before 5 April.

Child benefit charge — Income over £60,000 tapers child benefit; pension reduces adjusted net income.

Marriage allowance — Transfer unused allowance if partner is basic rate and you earn below allowance.

Model US comparisons for expats separately — this guide is UK-focused.

FiscalWise Tool Tie-In

US readers comparing systems can use tax bracket calculator for federal brackets; UK earners should pair this article with HMRC official tables each tax year.

Common Mistakes

Ignoring allowance taper — Bonus pushing £105k may cost more than face value.

Missing coding notices — Wrong emergency tax code after job change; fix via HMRC.

Not claiming WFH / professional subs — Where eligible on Self Assessment.

UK tax looks simpler than US until you hit £100k, dividends, or side business income. Know your bands, sacrifice salary to pension when marginal rate jumps, and file on time when PAYE is not enough.

Topics covered

- UK tax

- personal allowance

- income tax

- higher rate