Personal Finance in the Philippines: BIR Tax, SSS, and Building Savings

How TRAIN Law income tax works for Filipino employees, mandatory SSS and PhilHealth contributions, and practical savings with UITFs and emergency funds.

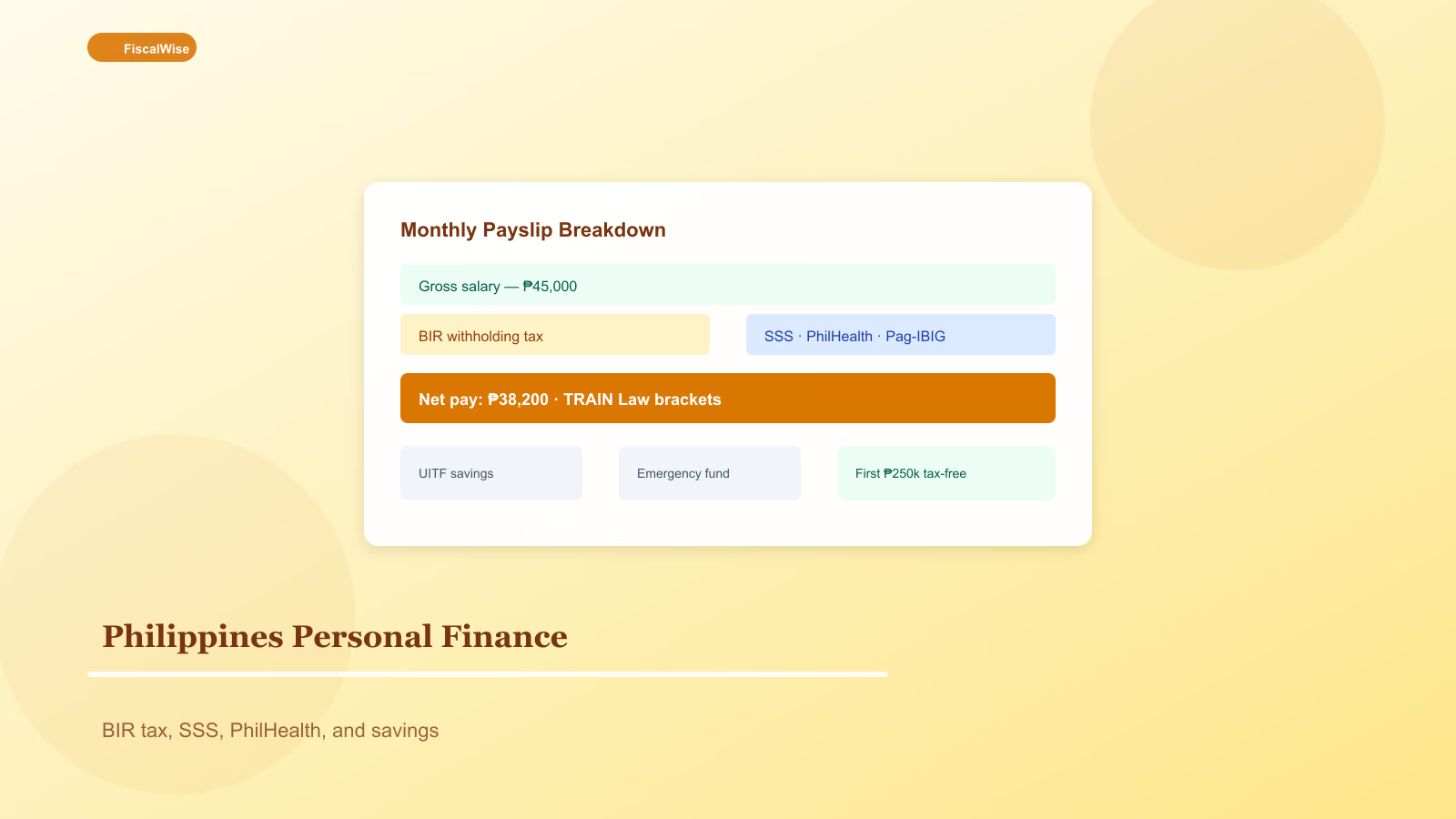

The Filipino Paycheck: What Gets Deducted

Salaried employees in the Philippines typically see withholding tax, SSS, PhilHealth, and Pag-IBIG deducted before net pay hits the account. Understanding each line helps you budget honestly and avoid treating gross salary as spendable income.

Withholding tax (BIR) — Your employer estimates annual income tax under the TRAIN Law and withholds monthly. True liability is reconciled when you file — or through annualised withholding adjustments.

SSS — Social security covering retirement, disability, and death benefits. Contribution rates and salary credit brackets update periodically; check the SSS website for current tables.

PhilHealth — National health insurance with shared employer-employee contributions.

Pag-IBIG (HDMF) — Mandatory savings fund that also supports affordable housing loans.

BIR Income Tax Brackets (TRAIN Law)

Annual taxable compensation income is taxed progressively:

| Taxable income | Rate |

|---|---|

| Up to ₱250,000 | 0% |

| ₱250,001 – ₱400,000 | 15% on excess over ₱250,000 |

| ₱400,001 – ₱800,000 | ₱22,500 + 20% on excess over ₱400,000 |

| Higher bands | 25% – 35% on larger incomes |

The first ₱250,000 of taxable income is tax-free — a meaningful benefit for entry-level and middle-income earners. Estimate your annual liability with our Asia-Pacific income tax calculator.

13th-month pay — Up to ₱90,000 of 13th-month pay and other benefits may be exempt. Amounts above the threshold are taxable.

Building an Emergency Fund in Pesos

Aim for three to six months of essential expenses — rent, groceries, utilities, minimum debt payments, and family support many Filipino households send home. Use our emergency fund calculator with PHP selected in the currency picker.

Park emergency cash in a separate savings account at a BSP-supervised bank. Avoid locking emergency money in time deposits you cannot break without penalty.

Savings Beyond the Bank: UITFs and Index Funds

UITFs (Unit Investment Trust Funds) — Offered by banks and trust departments; pooled funds with published NAVPU. Good entry point for index-style investing without picking individual stocks.

Mutual funds and ETFs — Available through licensed brokers and platforms. Compare fees (management, sales load, holding period) before committing.

Start with automatic monthly investments — peso-cost averaging through market ups and downs. Model long-term growth with our compound interest calculator.

Debt and Credit Discipline

Credit cards in the Philippines can charge 2–3% monthly interest if balances revolve. Run true borrowing cost through our credit card interest calculator. Pay in full when possible.

Personal loans and BNPL can smooth purchases but stack quickly. List every balance and rate; attack highest APR first using our debt payoff calculator.

OFW and Dual-Income Households

Overseas Filipino Workers often support family in the Philippines while earning abroad. Separate:

- Remittance budget — Fixed monthly support, not open-ended requests

- Personal emergency fund — In both host country and Philippines accounts if you maintain both

- Retirement savings — SSS voluntary contributions or host-country schemes where eligible

Convert foreign income to peso equivalents with the currency selector on any calculator before budgeting.

Year-Round Money Habits

- Track take-home pay after all mandatory deductions

- Automate savings on payday — even ₱500/month compounds

- File BIR Form 2316 from employer; keep records for annual filing if required

- Review SSS and Pag-IBIG statements yearly

- Increase investments when income rises — lifestyle inflation is the silent enemy

Philippine personal finance is mandatory contributions plus disciplined peso savings. Know your TRAIN tax bracket, fund emergencies in liquid pesos, and invest steadily through UITFs or index funds once the cushion exists.

Topics covered

- Philippines tax

- BIR

- SSS

- PhilHealth

- Filipino personal finance

Frequently Asked Questions

How much income is tax-free in the Philippines?

Under the TRAIN Law, annual taxable compensation income up to ₱250,000 is taxed at 0%. Income above that is taxed progressively at higher rates.

What is deducted from a Filipino salary besides tax?

Most employees see SSS, PhilHealth, and Pag-IBIG contributions withheld along with BIR income tax. Net pay is gross salary minus these deductions.

Is 13th-month pay taxable in the Philippines?

Up to ₱90,000 of 13th-month pay and certain other benefits may be exempt from tax. Amounts above the threshold are included in taxable income.

How should I start investing in the Philippines?

Build an emergency fund first, then consider UITFs or index mutual funds through licensed banks or brokers. Automatic monthly investments help with peso-cost averaging.