Income Tax and Savings in Pakistan: Slabs, Zakat, and Household Planning

How Pakistan's salaried tax slabs work for FY 2025–26, building rupee emergency funds, and National Savings schemes for conservative savers.

Pakistan's Progressive Income Tax (Salaried)

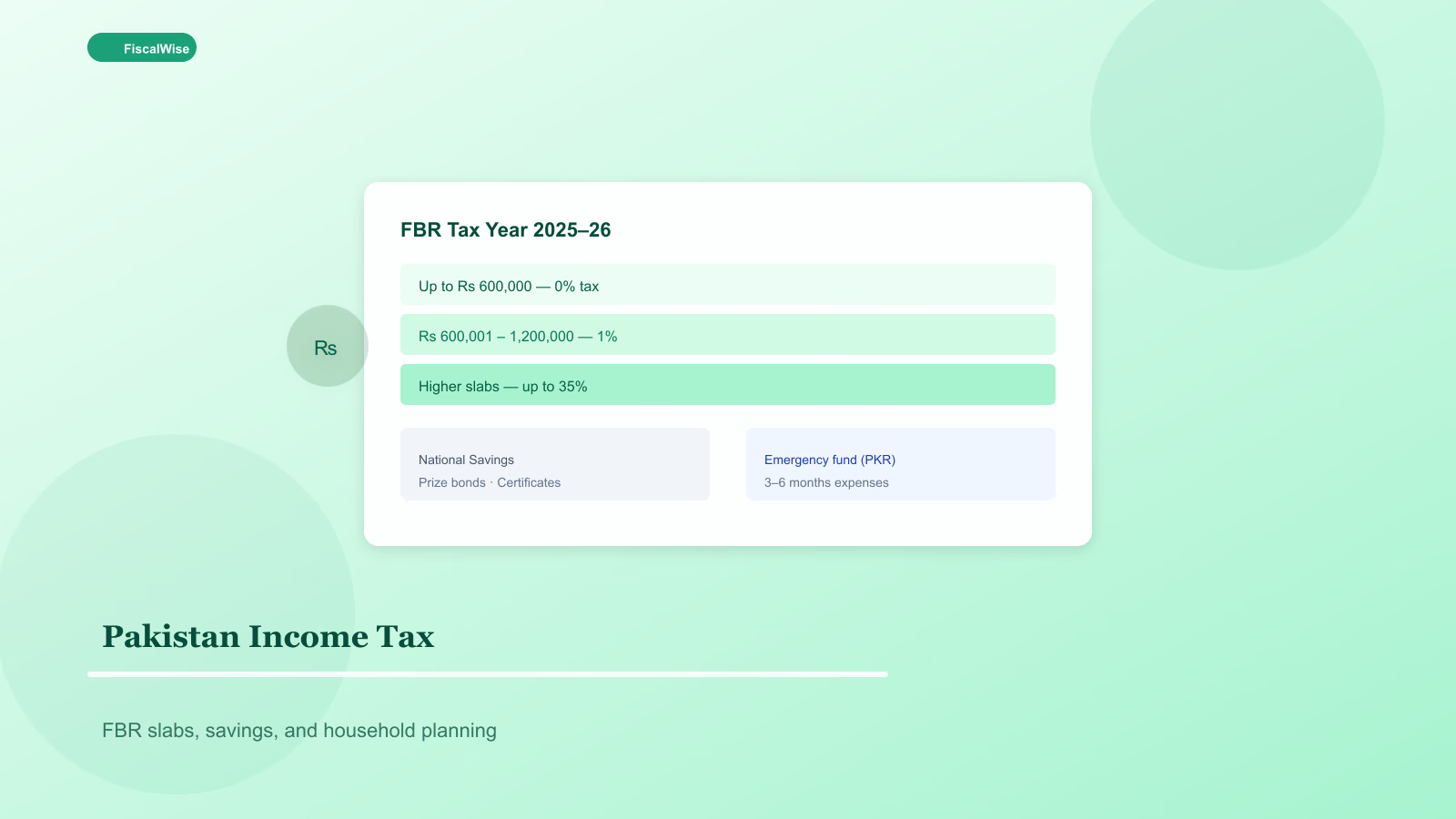

The Federal Board of Revenue (FBR) taxes salaried individuals on annual taxable income using progressive slabs. For tax year 2025–26, the structure broadly works as:

| Annual taxable income | Tax |

|---|---|

| Up to Rs 600,000 | 0% |

| Rs 600,001 – 1,200,000 | 1% on excess over 600,000 |

| Rs 1,200,001 – 2,200,000 | Rs 6,000 + 11% on excess over 1,200,000 |

| Higher slabs | 23% – 35% on larger incomes |

Employers withhold tax monthly under Section 149; reconcile through annual return filing if your circumstances change mid-year.

Estimate liability with our Asia-Pacific income tax calculator — select Pakistan and enter annual taxable income in PKR.

Taxable Income vs Gross Salary

Taxable income starts after allowable reductions — not every rupee on your offer letter is taxed. Common adjustments include:

- Zakat deducted where applicable

- Certain employer benefits treated differently

- Donations to approved charities (with documentation)

Consult FBR guidance or a tax adviser for complex cases — rental income, freelance side income, and business profits use different schedules.

Building an Emergency Fund in Rupees

Pakistani households face inflation and currency volatility. Keep three to six months of essentials — rent, utilities, groceries, school fees, transport — in liquid form before aggressive investing.

Use our emergency fund calculator with PKR currency. A separate bank account labelled for emergencies reduces accidental spending.

National Savings and Conservative Options

National Savings Schemes — Prize bonds, savings accounts, and term certificates through CDNS offer government-backed options familiar to conservative savers. Returns vary; compare real return after inflation with our inflation calculator.

Bank fixed deposits — Straightforward but taxable interest income. Useful for goals two to three years out, not emergency cash with penalties.

Equity and Mutual Funds

Licensed mutual funds and the Pakistan Stock Exchange offer growth exposure for long horizons. Rupee-cost averaging monthly — similar to SIP culture in India — reduces timing risk. Only invest money you will not need for five or more years.

Project growth with our compound interest calculator. Pair with our budget calculator to ensure monthly investments are sustainable.

Debt and Inflation Reality

Personal loans and credit cards at high APR consume cash flow. List balances and prioritise highest rates with our debt payoff calculator. Inflation erodes idle cash — balance emergency liquidity with investments that beat CPI over time.

Remittances and Dual-Income Planning

Many Pakistani households receive remittances from family abroad. Treat remittance as predictable income only if it is truly regular — not one-off gifts. Budget on local salary first; remittance funds goals and debt payoff.

Convert foreign amounts to PKR using the currency selector on calculators for apples-to-apples budgeting.

Practical Checklist

- Download annual tax card / employer certificate

- Estimate tax with calculator; adjust WHT if large refund or bill expected

- Automate monthly savings on salary day

- Keep emergency fund liquid in PKR

- File return on time to avoid penalties and enable refunds

Pakistan personal finance starts with understanding FBR slabs, keeping liquid rupee reserves, and investing surplus only after essentials and emergencies are covered. Tax planning and savings discipline compound quietly over years.

Topics covered

- Pakistan tax

- FBR

- income tax Pakistan

- savings Pakistan

Frequently Asked Questions

What is the income tax rate in Pakistan for salaried workers?

Salaried individuals pay 0% on taxable income up to Rs 600,000 per year, then progressive rates from 1% up to 35% on higher income bands for tax year 2025–26.

How is income tax paid in Pakistan?

Employers withhold tax monthly from salary under Section 149. You may need to file an annual return to reconcile total liability, claim refunds, or report additional income.

Where should I keep my emergency fund in Pakistan?

Keep three to six months of essential expenses in a liquid PKR savings account at a scheduled bank. Avoid locking emergency money in long-term certificates with penalties.

Are National Savings schemes safe?

National Savings products are government-backed and popular for conservative savers. Compare returns after inflation and tax on interest before relying on them for long-term wealth.